Founding an AI-Native Startup

From a painful workflow to a closed-loop company.

This chapter assumes you already know the machinery. You know the Agent Factory is the spec-driven, human-supervised process. You know its output is an AI-Native Company, and that the workforce inside it is made of Digital FTEs. You know the Two-Layer Model — human principals and their identic delegates at the Edge Layer, an AI Workforce Layer beneath. This chapter is not about how to build an agent. It is about how to build a company out of them, starting from nothing.

AI-Native Startup — a company designed from day one around Digital FTEs, evaluations, shared memory, and closed-loop feedback, either because it sells Digital FTEs to customers or because it runs internally on them.

Identic delegate — an AI agent that acts under a specific human principal's identity and authority. Together with the principals they answer to, identic delegates form the Edge Layer that supervises the AI Workforce Layer beneath.

AI-native service company — a company that sells a finished outcome rather than software, keeping its Digital FTE workforce in-house and delivering the work the way a law firm or audit practice does. The repricing this represents is called Service-as-Software.

Five-Level AI Maturity Ladder — this book's map of how far a company has gone with AI: (1) individuals experimenting, (2) the org standardizing on AI tools, (3) workflows redesigned around AI, (4) products with AI at the core, (5) the whole enterprise built out of AI. Levels 1–2 are adoption; Levels 4–5 are AI-native. (Developed in The AI-Native Transformation.)

A few terms used throughout — an eval is a repeatable test of whether an agent's output is genuinely good (correct, compliant, useful), not merely plausible. A DRI (directly responsible individual) is the one person who owns a cross-functional outcome end to end. An FDE (forward-deployed engineer) is an engineer who works inside the customer's company, on their systems, building the solution with them. Each is defined again at first use.

This chapter builds directly on the core machinery covered elsewhere in the book — the Agent Factory process, Digital FTEs, the Two-Layer Model, the system of record, and the eval loop. If any of those are still unfamiliar, read those chapters first; everything here assumes them.

📚 Teaching Aid

View Full Presentation — Found an AI-Native Startup

1. The Founding Window

There is a window open right now, and it will not stay open.

For most of software history, the founder's job was to assemble people. You raised money so you could hire engineers, so they could write code, so the code could become a product. Headcount was the unit of production, and everything downstream — your burn rate, your org chart, your speed — was a function of how many humans you could attract and coordinate.

That equation has been rewritten. The unit of production is no longer the engineer; it is the engineer in concert with a workforce of Digital FTEs, governed by memory and evaluations. A founder who understands this can manufacture, in weeks, what once took a funded team years.

This is not merely a mood in the market. Independent trackers estimate the agent-software category is growing several-fold across the second half of the decade, and Y Combinator's own thesis, argued repeatedly on its Lightcone podcast, is blunter still: vertical AI agents could be many times larger than the SaaS market that preceded them. Treat the exact multiples with suspicion — they come from people with reasons to be optimistic — but the direction is not seriously disputed.

What the window actually rewards is narrow and specific. The strategy this chapter teaches — find one painful workflow, go deeper into it than anyone else is willing to, and deploy a Digital FTE that owns it — works because the incumbents have not yet moved. On the Five-Level AI Maturity Ladder — experiment, standardize, redesign workflows, build AI-native products, run an AI-native enterprise — most of the companies you will compete against are stuck at Levels 1 and 2, handing every employee a copilot and calling it transformation. The founders who win this decade are the ones who treat that emptiness as a countdown rather than a comfort.

2. What an AI-Native Startup Actually Is

Most companies that say "AI" mean AI-assisted. They bolted a copilot onto a workflow designed for humans and left the workflow intact. The org chart did not change. The way decisions get made did not change. They got a faster horse.

An AI-Native startup is a different animal, and it shows up in two distinct forms that are easy to confuse. It is worth separating them now, because the rest of this chapter draws on both.

The first is the AI-Native company as a product: you build and sell Digital FTEs to other organizations. Your product is a worker. Salient sells a loan-servicing agent; HappyRobot sells a freight-operations agent; Reducto sells the document-processing layer that other people's agents depend on. The customer rents a workforce they could not build themselves.

There is a sharper, more aggressive version of that first form, and it is where some of the decade's largest markets sit. Instead of renting the workforce to the customer, you keep the workforce and sell only the finished outcome — the completed tax return, the reviewed contract, the approved filing, the resolved claim. The customer never sees a Digital FTE. They see a result, delivered to a standard, on a deadline, exactly as they would from a law firm or an audit practice today. This is the AI-native service company, and the repricing it represents already has a name: Service-as-Software, the move from selling a tool the customer must operate to selling the work itself, developed in The AI-Native Transformation. Y Combinator argues that some of the biggest companies of the coming decade may not be software businesses at all, but service businesses — insurance, tax, audit, mortgages, law, parts of healthcare and logistics — rebuilt from scratch around Digital FTEs. The pull is arithmetic: these markets are measured against the labor budget, in the trillions, not the software budget, in the billions. The service company is the form this chapter returns to most often, because its market selection, its pricing, and its margin structure follow rules a pure software company never has to face.

The second is the AI-Native company as an operating model: you run your own company as a closed-loop intelligence, with Digital FTEs woven into how decisions actually get made internally. This is the model Jack Dorsey and Sequoia's Roelof Botha describe in their 2026 essay From Hierarchy to Intelligence — a company organized as an intelligence rather than a hierarchy, which they go so far as to call a "mini-AGI" (Block, 2026).

These are different answers to different questions — what do I sell? versus how do I operate? The reason this chapter covers both is that the same discipline underwrites each: specifications both humans and agents can read, evaluations that define quality, a system of record the workforce can query, and human accountability held at the Edge Layer. A founder who masters that discipline tends to do both at once. The company you build to sell Digital FTEs is itself run on Digital FTEs. The factory makes the product and runs the firm.

Underneath both forms sits a single architectural commitment, and it belongs at the center of your vision. The idea comes from control systems. An open loop acts and never checks the result — like a heater you switch on and leave running, whatever the room does. A closed loop senses the result and keeps adjusting — like a thermostat that reads the temperature and corrects toward the setting you want. A legacy company runs as an open loop: information lives in people's heads, in unwritten meeting notes, in side channels, in the vague institutional sense of "how we do things." Decisions are made on lossy inputs, error accumulates quietly, and the system drifts. An AI-Native company runs as a closed loop: every artifact the company produces is readable by the workforce, every outcome feeds back, and the loop corrects itself. The advantage you have as a founder is that you do not have to retrofit this. Incumbents must dismantle centuries of hierarchical habit to reach it; you can be born closed-loop.

Hold both forms in view as you read on, because they organize what follows. The wedge, the go-to-market, the pricing, and the growth curve speak first to the founder selling Digital FTEs, since that is the path most founders take first. The founding shape is where running your own company as an intelligence comes forward. The factory and the moat belong to both. Where the path forks between the two, this chapter marks the fork.

The path from here looks like this:

3. Finding the Wedge

You do not start with a market. You start with a workflow.

That workflow is your wedge: the single narrow problem you use to get your first foothold in a market — the way a thin wedge can split a heavy log, because all of its force lands in one place.

The mistake first-time AI founders make is to pick a category — "legal," "healthcare," "logistics" — and try to build a platform for it. A category is too big, too defended, and too abstract for a Digital FTE to own. What you want instead is a single, painful, unglamorous, high-friction process, the kind that today runs on phone calls, email threads, spreadsheets, and people staying late. Garry Tan describes the founders who win as acting almost like ethnographers, exploring the underserved slices of the GDP pie chart. You are not looking for a big idea; you are looking for a small, expensive, deeply annoying piece of work that nobody has bothered to automate because it was too messy to digitize.

Three tests tell you whether a workflow is a real wedge.

It must be messy enough that generic models fail. If a general-purpose assistant can already do it, you have no moat. The friction — the domain rules, the edge cases, the regulatory nuance — is the thing that protects you.

It must be narrow enough that a deployed solution wins. You should be able to point at one outcome and own it end to end, rather than gesture at a category.

It must be painful enough that someone pays this quarter. Not "would be nice." The kind of pain that survives a budget review.

The domain knowledge required to find such a wedge is itself the moat, and you can acquire it deliberately. The founders of HappyRobot did not come from freight; they came from robotics and computer vision, then went into the operational guts of logistics until they understood it cold. Their CEO, Pablo Palafox, has argued that being verticalized beats general-purpose voice startups that are, in his words, clueless about the operations and intricacies of these industries. Salient's founders did not come from consumer lending either; they learned it by living in it. The lesson is not "have a background." It is to go and get one, on purpose, in a domain that is not in the training set.

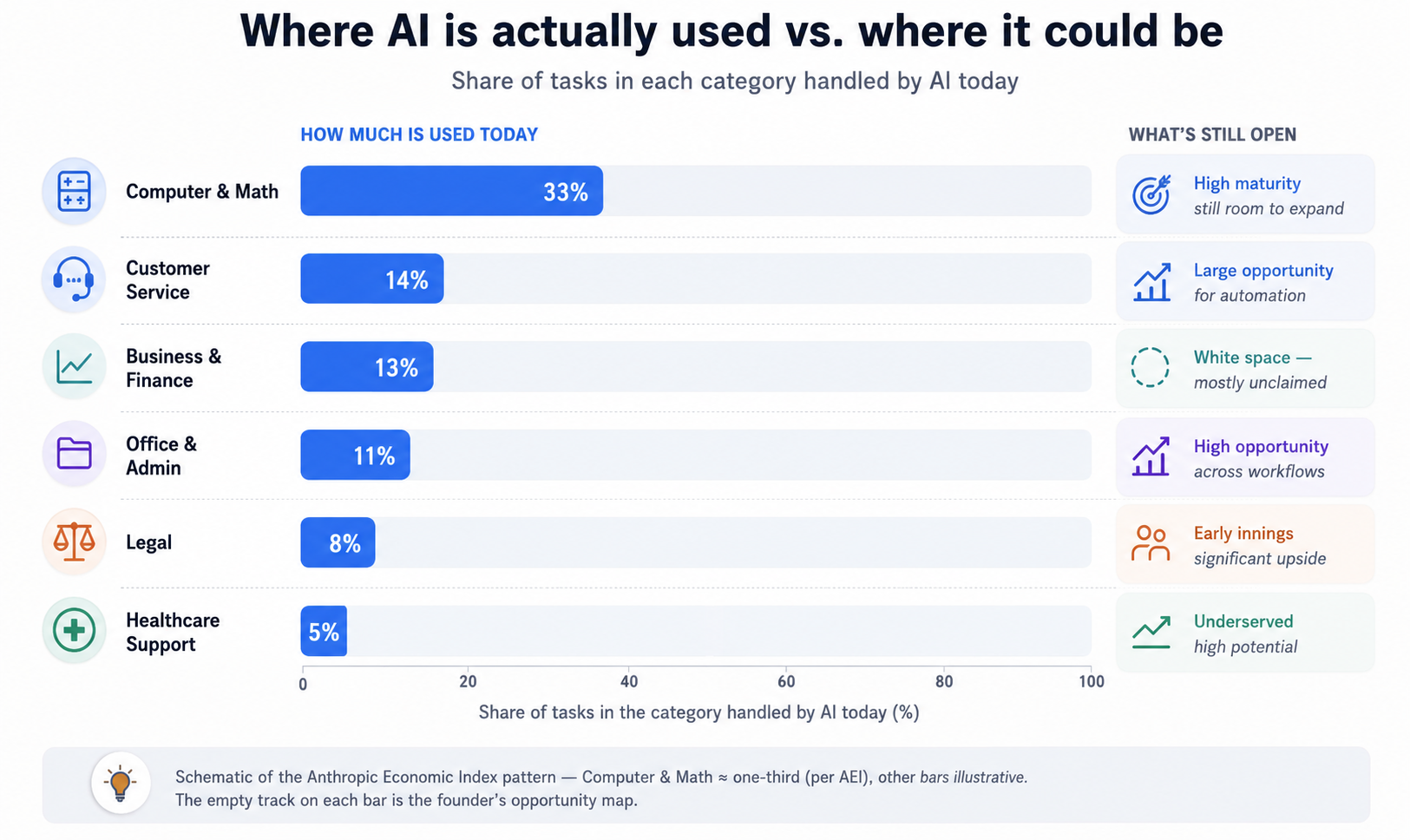

To find the open ground, read the map honestly. Anthropic's Economic Index, built from real anonymized usage of Claude, shows that AI adoption is strikingly uneven — concentrated in a handful of countries and occupations. Even in the most-penetrated category, Computer and Math, observed usage covers only about a third of the tasks the models could theoretically perform, and usage across the economy still leans toward augmentation rather than full automation (Anthropic Economic Index, 2026). Translate that for founding purposes: the territory where work is genuinely being handed off to agents is small, and the white space — finance back-offices, legal operations, claims processing, customer service, and the rest — is mostly unclaimed. That gap is your opportunity map.

The filled bars show how little of each category's work is handed to AI today; the empty track on each bar is the founder's opportunity map.

The filled bars show how little of each category's work is handed to AI today; the empty track on each bar is the founder's opportunity map.

The Service-Market Lens

The three tests above hold for any wedge. When the wedge is a service — work a customer already pays an outside vendor to do — Y Combinator's playbook for AI-native service companies, presented by visiting partner Charlie Warren, adds four traits that separate a great service market from a punishing one. Two of the four are the service-market form of tests you have already met: the whole job is genuinely hard restates messy enough that generic models fail, and judgment is concentrated restates narrow enough that a deployed solution wins in the language of task decomposition. The other two — already outsourced and regulation as moat — are new, and specific to the act of displacing a vendor. Score a candidate market against all four.

The work is already outsourced. The strongest service wedges are low-trust in a precise sense: the customer already hands the work to a vendor and judges only the final product, not how it was produced. You are displacing a supplier, not changing a behavior — you show up where the budget already lives and do the work. No behavior change is the cheapest growth there is, and an entrenched outsourced line item gives you exactly that.

Judgment is concentrated, not spread. Decompose the work. If every sub-task needs a human exercising real judgment, you have rebuilt a staffing agency and you will not scale. You want most steps automatable, with human judgment pooled in the few places where it genuinely belongs. This is the 10-80-10 rhythm applied to a market rather than a single agent: thin human intent up front, a wide band of agent execution, a final layer of human verification on the output.

The whole job is genuinely hard. This sounds like it contradicts the previous trait; it does not. The overall outcome has to be difficult enough that models and humans are both required to produce something the customer will accept. Trivial work commoditizes and draws a hundred competitors; difficulty is a moat. The art is a job that is hard in aggregate but decomposes into mostly-automatable parts.

Regulation can be the moat. Founders instinctively avoid regulated markets. For a service company, regulation often works in your favor: higher expectations and legal accountability raise the bar, and the bar is the wall that keeps the next entrant out. A market that punishes sloppy output rewards a workforce engineered for consistency. Panacea, a YC company, sits on all four traits at once — it delivers AI-native FDA regulatory services for biotech and medical-device companies, a market that is already outsourced, decomposable into structured drafting and synthesis, genuinely hard and consequential in aggregate, and heavily regulated. It pairs the most experienced ex-FDA consultants in the industry with an AI platform; the consultants are not the product — they are the human verification layer on a workforce that does the volume (Y Combinator, 2026).

One durability test belongs on top of the four. YC calls it the Sam Altman test — borrowing the name, and distinct from the one-person-billion-dollar-company prediction this book attributes to Altman elsewhere: as the models get better, does your service get stronger, or does the model commoditize you? You want to be firmly in the first camp — where every model improvement makes your Digital FTEs cheaper, faster, and more capable while your domain knowledge, your data, your regulatory moat, and your operational discipline stay yours. A company whose entire value is the model will be erased by the model. A company whose value is a system of record uses the model as fuel and compounds as the fuel gets cheaper. It is the same principle this book states elsewhere as the method is the constant, the tool is the variable — here turned into a market-selection filter.

There is a tempting shortcut, especially for founders with an operating background: acquire an existing services firm, bolt AI on top, and short-circuit the revenue ramp. With one exception, this is a trap. You cannot acquire product-market fit, and you cannot acquire an AI-native culture — a legacy services business arrives with legacy expectations on metrics, hiring, and what "good" looks like, and AI on top changes none of them. The one defensible reason to buy is to acquire a regulatory moat quickly — an insurance license, say, where the alternative is years of process. Outside that narrow case, building beats buying almost every time. You are constructing a new kind of operation; start it as one.

A final note on where not to look: be wary of services that depend on equipment and on-site physical labor. The margin math here assumes software-like leverage, and it breaks the moment you own and operate physical things — you inherit the cost structure of the physical world. Those can be excellent businesses; they are simply not this one. Leave that ground to the robotics founders.

The Framework Travels

Notice that nothing in the four traits is specific to Silicon Valley. The case studies in this chapter are American because that is where the press coverage sits, but the tests themselves are geography-free. Run them on almost any outsourced service, in any market — medical-billing and revenue-cycle work, statutory and tax-compliance filings, back-office reconciliation, claims adjudication, contract and document review. Each is typically already outsourced; each decomposes into mostly-mechanical steps with judgment concentrated in a final review; each is genuinely hard in aggregate because the rules are dense and keep changing; and each sits behind regulation that punishes errors. That is four-for-four, and it holds on any continent. The wedge framework is not a Bay Area artifact — it is a way of reading any economy's outsourced work, and the founder closest to that work, wherever they sit, holds the domain advantage this chapter keeps insisting on.

Here is the chapter's first fork. If your aim is the operating-model company rather than a product to sell, run the same exercise inward. Your first wedge is the most painful workflow inside your own walls, and the first Digital FTE you deploy is one you will never invoice for. The discipline is identical; only the customer changes.

4. The Founding Shape

The AI-Native company can be flatter from the first day, and the flattening is structural rather than cultural. It does not remove leadership, governance, compliance, product judgment, or customer ownership — those stay firmly at the Edge Layer. What it removes are the layers that exist only to route information.

Hierarchy exists to move information. For two thousand years — Dorsey and Botha trace it to the Roman army — organizations have inserted layers of middle management whose real job is to route information, pre-compute decisions, and hold alignment across a group too large for any one person to see. When the workforce becomes a closed loop with a shared world model, that routing function can be performed by the system itself. The middle layer is not cut to save money. Once the system moves the information on its own, that layer is simply no longer needed.

In practice this collapses the company into three roles, and they map almost exactly onto your Two-Layer Model. There is the individual contributor, a deep specialist who takes direction from the model rather than a manager, and who is rarely working alone — even a salesperson now orchestrates a pipeline of Digital FTEs. There is the directly responsible individual — the DRI, borrowed from Apple — who owns a cross-functional outcome end to end and has standing permission to pull whatever the workforce can provide. And there are the human principals who live, in Dorsey and Botha's phrase, "at the edge" of the organization, handling the creative, cultural, and ethical decisions that cannot be delegated while the AI Workforce Layer handles coordination.

That last role is your Edge Layer, named by someone else and arrived at independently. When a payments company restructuring under duress and a startup blueprint built from first principles converge on the same shape, it is a strong sign the architecture is right.

The mechanism that makes this work is a system of record. Dorsey and Botha describe it as a world model that tracks every decision, discussion, plan, and problem, paired with a strong customer signal that defines success. This is the same instinct that makes a queryable, agent-readable system of record the spine of an AI-Native company: the DRI orchestrates, the world model remembers, the customer signal judges, and there is no manager in between because none is needed.

This is also where the new headcount math becomes a design constraint rather than a slogan. Salient reportedly reached meaningful scale with roughly forty employees, weighting its hiring toward engineering and, by its CEO's emphasis, prioritizing real revenue over a paper valuation. Reducto, in its early days, ran with a famously small team. Revenue per employee stops being a vanity metric and becomes a number you set: you are not trying to grow the org chart, you are trying to keep it small while the workforce beneath it scales. Block treated this as more than theory — in early 2026 it cut roughly four thousand of more than ten thousand employees and framed the move not as cost-cutting but as a permanent restructuring to replace middle management with intelligence. That is an incumbent paying, in pain, for a transition you can skip.

5. Build: The Factory Is the Company

The mechanics of manufacturing a Digital FTE — the spec-driven, human-supervised loop of Manufacture, Package, and Monetize — are the subject of the rest of this book (see the Agent Factory build chapters), and the founding context does not change them. What it changes is their scope. For a single agent, the skill–resolver–memory–evaluation loop is how you build one reliable worker. For a company, that same loop is the operating system of the entire business: it is how the product gets made and how the firm runs itself.

This has a consequence founders underrate. The factory is not a phase you complete before going to market; it is the thing you are selling and the thing you are becoming, simultaneously. Your evaluation suite is both your quality gate and your moat. Your system of record is both the product's memory and the company's. When you treat the factory as infrastructure rather than a build step, the two forms of AI-Native company from Section 2 stop being separate projects and become one.

When the company is a service, this loop takes a particular shape, and it inverts the instinct most software founders carry. In ordinary software the product is the interface and the human is the user. In a service company the human expert is the interface to the customer, and the product is the system that lets that expert's judgment scale nonlinearly. The customer talks to a person and receives an outcome; behind the person is a workforce of Digital FTEs doing the volume. Two consequences follow. First, throughput and cycle time become product metrics — you track them the way a SaaS company tracks daily active users, and the roadmap becomes a list of bottlenecks to relieve rather than features to ship. General Legal, the AI-native law firm built by the team behind Casetext, treats this literally: it engineered shift work into how it serves clients, compressing turnaround to hours and, as a side effect, attracting strong lawyers who want sane hours (Y Combinator, 2026). Second, the humans in the loop must scale nonlinearly — if revenue rises in lockstep with headcount, you have built a consultancy with a chatbot, and you will hit the ceiling every services firm hits. The whole bet is that one supervised human ships the output that used to take ten.

Before going further, internalize the one line that separates a company from a science fair: the line between a demo and a deployment. A demo is easy, and the market is now drowning in them. Getting a Digital FTE to production — reliable on real data, on the customer's worst day, inside their actual systems — is the hard, unglamorous, company-defining work. The penalty for skipping it is well documented: Gartner predicts that more than 40% of agentic AI projects will be canceled by the end of 2027, citing escalating costs, unclear business value, and inadequate risk controls (Gartner, 2025). Read the figure as a forecast, but read the pattern as real. The failures are rarely failures of model quality; they are failures of discipline — shipping the demo, calling it done, and watching it fall over. The eval-gated, test-covered rigor the Agent Factory imposes is the direct answer. A demo proves the model can; a deployment proves the workforce will, repeatably.

6. The Moat: Taste, Evals, and the Closed Loop

When the cost of writing code falls toward zero, every founder has to answer one question: what is left to defend?

The increasingly agreed-upon answer is taste expressed as evaluations. An evaluation — an eval — is a repeatable test that checks whether an agent's output is genuinely good: correct, compliant, and useful, not merely plausible-sounding. Garry Tan has called evals the real moat for AI startups — not the model, not the prompt, but the capacity to measure quality systematically. OpenAI's Greg Brockman has said that evals are often all you need, and the investor Anjney Midha has pointed out the tell: the best AI product leaders publicly credit "taste" as their differentiator, while behind the scenes it is relentless evals. Tan connects the two directly — taste is the thing the model has not solved and may never fully solve, and it shows up operationally as the question of whether a given prompt, model, and Digital FTE actually hold up across the scenarios a real customer will throw at them.

This is why generic benchmarks are a trap. A high score on a public benchmark tells you nothing about whether your Digital FTE preserved a customer's trust, followed the domain's rules, or hit the business goal. The only judge that matters is the user, in your specific domain, on your specific workflow — and because that judgment differs in every vertical, it cannot be commoditized away by the next model release.

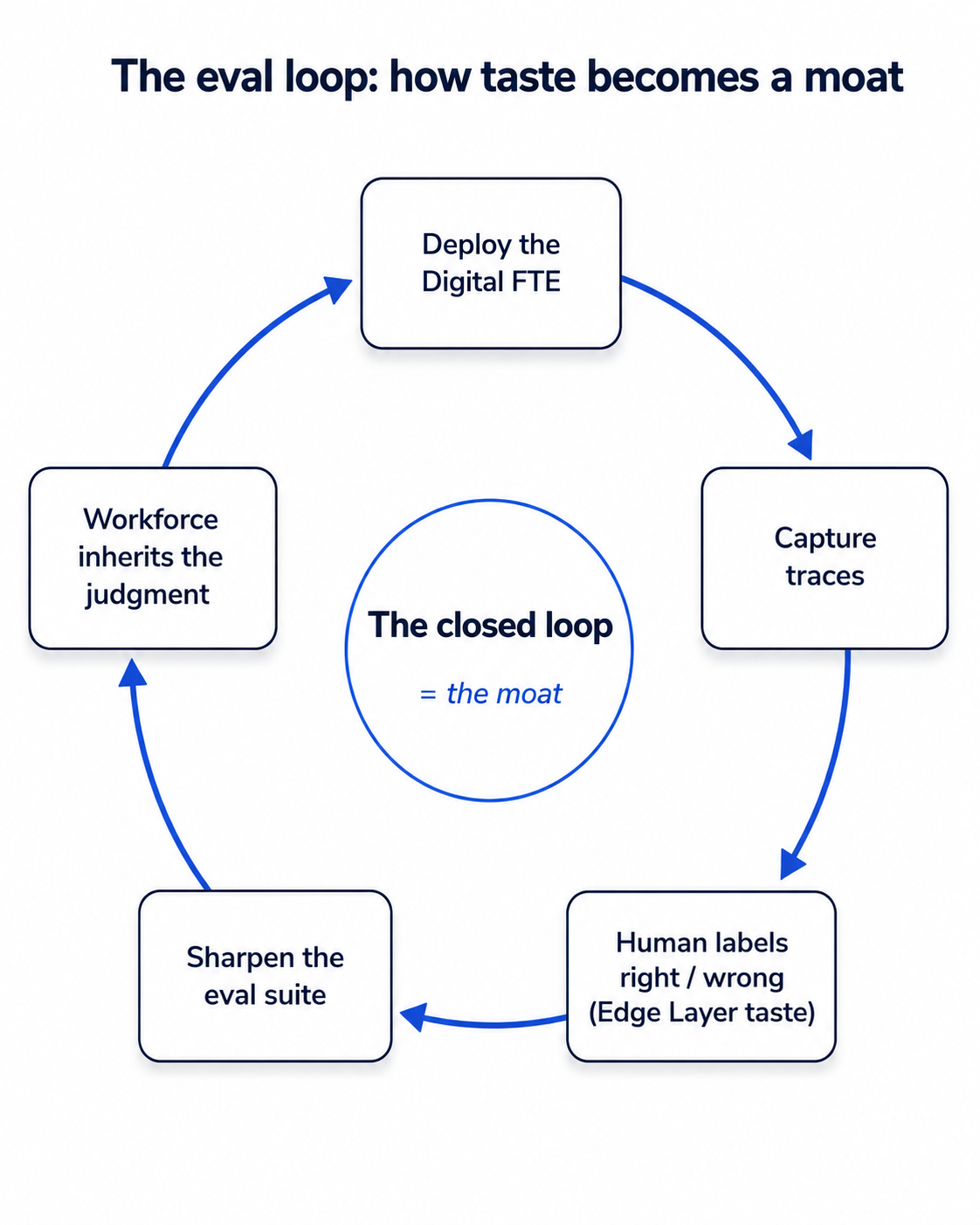

So the founder's non-delegable work is to sit with the traces: to read what the workforce actually did, label it right or wrong, and feed that judgment back into the loop. This is the closed loop made personal — the human at the Edge Layer supplies the taste, the eval suite encodes it, and the workforce inherits it. It is tedious, it is the moat, and it is one of the Seven Invariants made concrete. Human accountability does not get automated, even in a company built of automated workers.

Taste becomes a moat when it is encoded as evaluations and fed back through a loop the workforce inherits.

Taste becomes a moat when it is encoded as evaluations and fed back through a loop the workforce inherits.

Variance Is the Existential Threat

There is a reason the eval suite earns the word existential in a service company, and it is worth stating as bluntly as the founders who learned it the hard way:

Customers will fire you for variance faster than they will fire you for being a little slower or a little more expensive than the incumbent.

By variance we mean non-uniform output — the return that is excellent on Tuesday and wrong on Thursday. The vendor you are displacing is trusted, and trust is built entirely on consistency. Inconsistency destroys trust, and lost trust is churn that no amount of speed or price will win back. This is why the eval loop is not hygiene; it is the machine that holds variance down to a number a customer will tolerate, and — if the illustrative figures from this book's own comparison hold — the difference between the rough 85–95% consistency of a human team and the 99%+ a well-built Digital FTE workforce can reach. Treat those numbers as targets to engineer toward, not measured guarantees. In a service market, predictability is the product. The founder who internalizes that ships evals before features — and the one who does not learns about variance from a cancelled contract.

7. Go-to-Market: Deploy, Don't Demo

The most important strategic word in this chapter is deploy.

The companies posting growth numbers that sound impossible are not selling AI in the abstract; they are deploying full solutions inside a customer's messiest workflow and owning the outcome. The motion that makes this work has a name and a lineage: the forward-deployed engineer.

Put plainly: a forward-deployed engineer is an engineer you send to work inside the customer's own company — sitting with their team, on their own systems — building the solution together with them, instead of shipping them software and leaving them to install it alone.

Palantir — a data-software company known for its work with governments and large enterprises — invented it in the early 2010s, when its intelligence-community customers could not even articulate their problems in a product brief. The only way to solve them was to embed engineers — Palantir called them "Deltas" and "Echoes" — directly inside the customer's organization, sometimes for months, to learn the domain, stitch the systems together, and ship working software on the customer's own ground. The internal philosophy was "gravel road to paved highway": the embedded engineer builds a fast, rough, customer-specific solution, and the core team studies it, finds the pattern across customers, and turns it into product. a16z now calls the forward-deployed engineer one of the hottest roles in tech (a16z, 2026), and in May 2026 both OpenAI and Anthropic formalized the model at scale — OpenAI launching its own Deployment Company, capitalized at more than four billion dollars and seeded with roughly 150 forward-deployed engineers through its acquisition of Tomoro, and Anthropic standing up a parallel forward-deployed venture and co-building embedded agent systems with enterprises such as FIS (OpenAI, 2026).

For a founder, the actionable claim is that the forward-deployed engineer belongs in your first handful of hires, ahead of your first salesperson. The reason is the compounding loop. A sales-led motion produces a closed deal and a note in a CRM. A forward-deployed motion produces a closed deal and a piece of product and a piece of domain knowledge that makes the next deployment faster. Proponents put the iteration advantage at several times a traditional sales motion; even if you discount that, the structural point holds — every engagement feeds the product instead of dead-ending in an account record.

The case studies are the playbook. HappyRobot funds a dedicated forward-deployed engineering team that works on-site to tailor its agents to each freight operator's reality. Salient lands customers through a deliberately narrow pilot — one loan portfolio, one agent, clear guardrails, measurable outcomes in weeks — and then expands. That is your template: win one workflow inside one customer completely before widening by an inch.

The narrow pilot is also a defense against the most common way these companies die young. When you are new and have nothing, pilots are easy to sign — and the temptation is to sign a lot of them. But pilots you cannot serve will bury you: to keep early customers happy you throw humans at delivery, and while you are buried in manual delivery you have no time to build the product that was supposed to automate it. You get stuck running on people. Cap your first pilots to a small handful, treat them as the place you learn where AI gives you unique leverage rather than where you standardize too early, and sell the outcome — not seats, not tokens. The pilot is the product.

One honest caveat, and it comes from a16z itself: the forward-deployed model works only when there is a real platform underneath the bespoke work. Embed without a product engine behind you and you become a consulting shop that happens to use AI — trading hours for money with no compounding asset. The forward-deployed engineer is a flywheel for the product, not a substitute for it.

Forward deployment is not consulting if every engagement improves the product, the eval suite, and a reusable workflow specification. If each customer instead requires a one-off rebuild that compounds into nothing, you are running an agency with extra steps.

Picture a team that builds a sharp claims-processing agent for one insurer, then rebuilds it almost from scratch for the next because none of the first build became a reusable spec. Three customers in, they have three fragile codebases, no product, and a calendar consumed by maintenance — busy, paid, and going nowhere.

8. Monetizing the Workforce

Here the two forms of AI-Native company part ways, and the fork is worth naming. If you are selling Digital FTEs, monetization is your revenue model — the price a customer pays to rent a worker. If you are running your own company on Digital FTEs, "monetization" is really margin: the worker shows up not as a line of revenue but as a cost that never arrives — a profit margin that a competitor carrying many human salaries cannot match. Both are real business models. This section is about the first; the second is simply the discipline of the founding shape, expressed on the income statement.

Whichever you are building, the anchoring principle is the same: price against headcount, not against software. A Digital FTE that replaces or augments human labor should be valued against the fully loaded cost of that labor, not benchmarked against a per-seat SaaS comparison. The case studies justify it. Salient's agents reportedly automate the large majority of outbound calls while measurably improving payment rates, and one public deployment cited a reduction in call handle times of more than sixty percent. Those are outcome metrics, and they support a value-based contract far better than a seat license can.

For a service company the anchor is sharper still: you are not competing with other software vendors, you are competing directly with the cost of labor, internal or outsourced. Two ways of expressing that price tend to work. Per-unit pricing — per return, per claim, per loan, per contract — is the cleanest and the easiest to explain, because it maps onto the customer's existing sense of what one unit of the outcome costs; General Legal prices contract review at a flat fee per document rather than by the billable hour. Outcome pricing ties payment to the result and aligns incentives beautifully, though it is harder to forecast on your own side; Panacea bills on the completed consultant study against milestones rather than by the hour, which is itself a signal that it sells outcomes. Two pricing approaches reliably destroy value and should be avoided: cost-plus, which caps your upside permanently and hands your operating leverage straight to the customer, and straight-line undercutting, which frames your work as cheap and therefore — in a market that just fired a vendor for variance — suspect. Price on value, not on being the discount option.

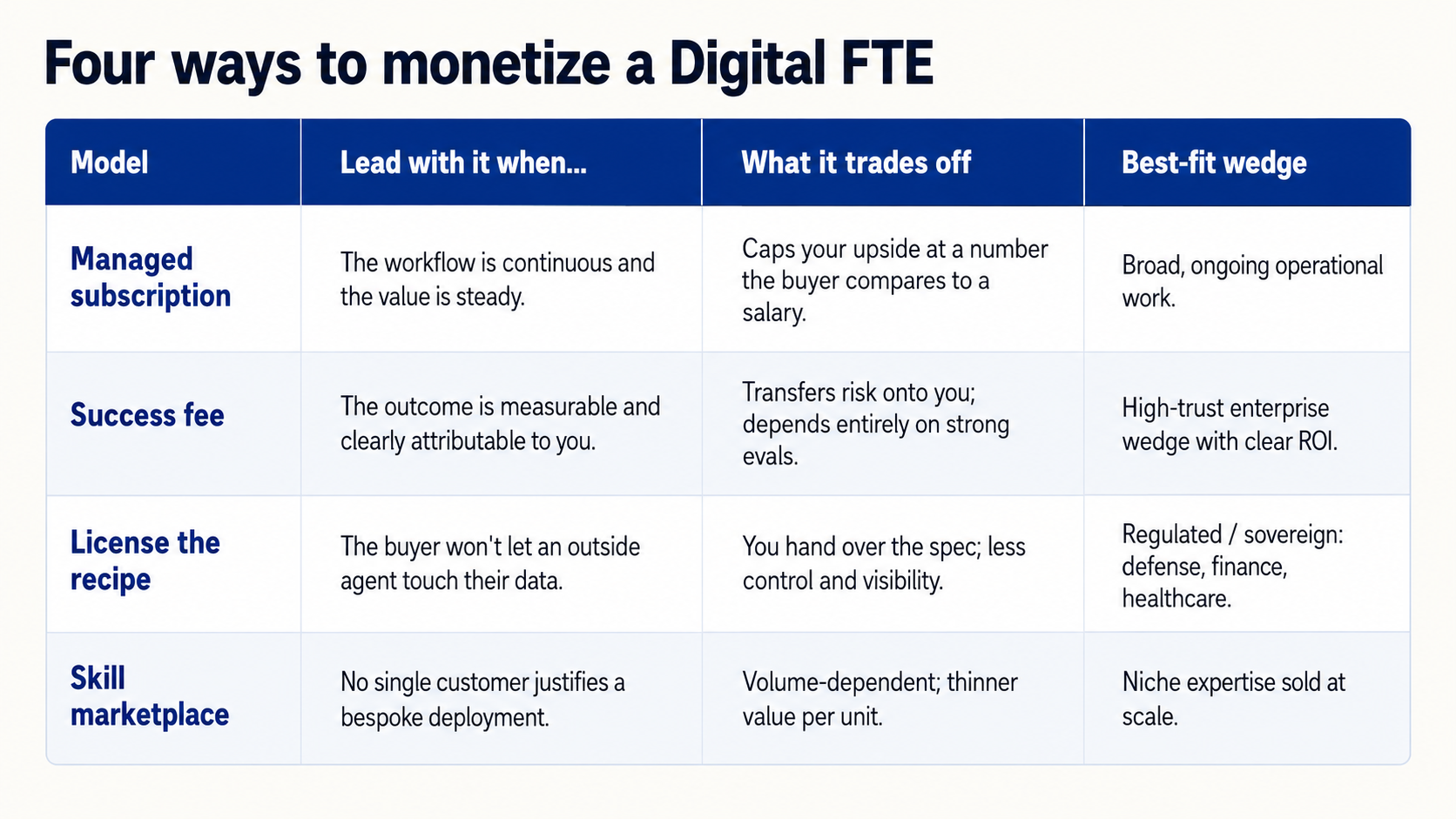

The book's four models are not interchangeable; each fits a different shape of wedge. The managed subscription is the easiest to sell and the easiest to forecast, but it caps your upside at a number the buyer can rationalize against a salary line — reach for it when the workflow is continuous and the value is steady. The success fee can capture far more of the value you create and puts your incentives on the same side as the customer's, which is why it often closes fastest in a high-trust enterprise wedge; but it works only when the outcome is measurable and attributable, which means it rests entirely on the evaluation and instrumentation discipline from the moat. It also transfers risk onto you, so reserve it for wedges where you are genuinely confident in the worker's reliability. Licensing the recipe — selling the specification and letting the customer run it inside their own walls — is the model for regulated, security-sensitive, or sovereignty-conscious buyers in defense, finance, and healthcare who will not let an outside agent touch their data. The skill marketplace is for niche expertise at volume, where no single customer justifies a bespoke deployment.

Each model fits a different shape of wedge; lead with the simplest one the wedge will bear.

Each model fits a different shape of wedge; lead with the simplest one the wedge will bear.

Lead with the simplest model the wedge will bear, and let the relationship — and your accumulating eval evidence — earn you the right to value-based pricing over time. The most common founding mistake is the opposite instinct: anchoring low against the human comparison out of fear, charging for the seat, and only later discovering that the buyer would gladly have paid for the outcome.

9. Growth and Scaling

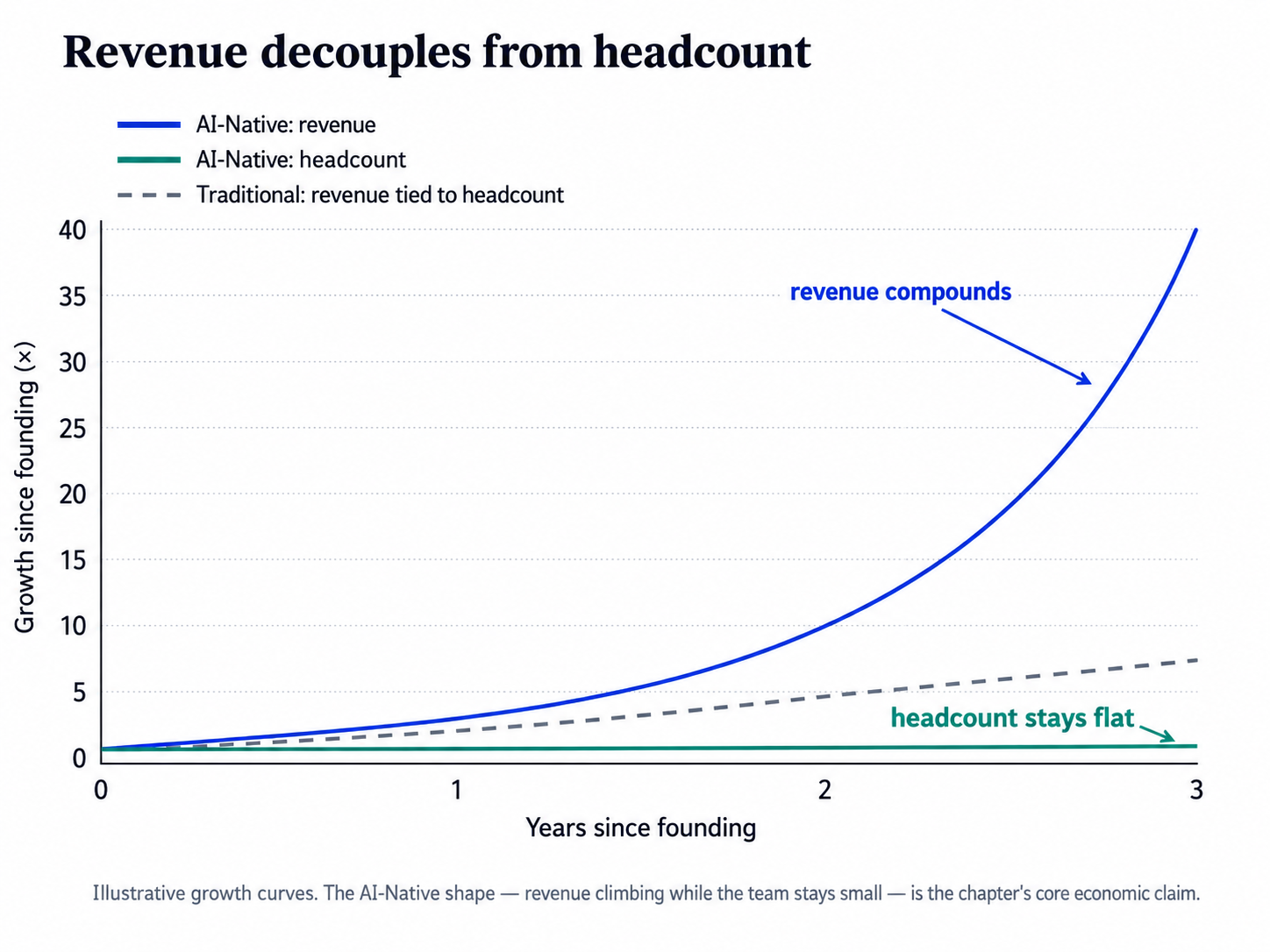

The growth curve of an AI-Native company looks wrong to anyone trained on the old math, because it decouples revenue from the size of the team producing it.

The trajectories are now a matter of record — though every figure below is self-reported or press-reported as of early 2026, so read them for the shape of the curve, not the decimal. Salient reportedly reached roughly twenty-five million dollars in annual recurring revenue in about two years, and did so without losing a customer along the way. HappyRobot grew its revenue more than tenfold between funding rounds, well into the eight figures, while expanding to more than seventy enterprise customers — DHL, Ryder, Schneider, Werner — within roughly a year of going to production (Reuters, 2025). Reducto raised about $108 million across two rounds in a single year (a $24.5M Series A and a $75M Series B) as the document layer that other AI companies build on, its monthly processing volume multiplying more than sixfold between rounds as it processed close to a billion pages (Reducto, 2025).

Illustrative growth curves. The AI-Native shape — revenue climbing while the team stays small — is the chapter's core economic claim.

Illustrative growth curves. The AI-Native shape — revenue climbing while the team stays small — is the chapter's core economic claim.

What matters more than the numbers is understanding which parts of the machine scale and which do not. The Digital FTE workforce clones almost instantly and almost for free — that is the exponential, and it is real. The founder's taste and the eval suite that encodes it do not clone; they are the bottleneck, and they are supposed to be. The discipline of scaling an AI-Native company is to scale the loop — more deployments feeding more traces feeding a sharper eval suite — without letting the org chart underneath it grow in proportion. The workforce expands; the Edge Layer stays small and sharp.

10. The P&L and AI Operating Leverage

The growth curve in the previous section is what an AI-Native company looks like from the outside. The profit-and-loss statement is what it looks like from the inside, and for a service company it is where the business is won or lost. The structure is standard — revenue minus cost of goods sold gives gross profit; gross profit minus operating expenses gives operating income — but each line behaves differently when the workforce is mostly AI.

Revenue is the comparatively easy part: you will be able to sign contracts. The hard question is whether you can deliver on them repeatably, and early on revenue will be spiky month to month. That is normal; a maturing product-process smooths the lumpiness over time.

Cost of goods sold (COGS) is where you obsess from day one, because it is the line AI operating leverage acts on. In a service company COGS has three components, and each needs a number, a trend line, and a named owner. Model cost is the inference and API spend per unit of work, and its owner watches cost-per-outcome trending down as the frontier commoditizes. Hosting cost is the infrastructure the workforce runs on, watched to scale sub-linearly with volume. And humans in the loop — the verification and judgment layer — are tracked by outputs-per-human, which should trend up as the product absorbs more of the work.

Be deeply suspicious of zero-margin or negative-margin pilots. They are fine to learn from; they are dangerous to get hooked on. Operating expenses are the familiar ones — R&D to build the product, plus sales, general, and administrative — and operating income is what remains after COGS and OpEx. You will be judged on operating income sooner than you expect; net income, after taxes and interest, matters less in the medium term.

The core bet of the entire model lives in how those COGS lines move over time:

AI operating leverage: the more product you build, the lower the COGS, the better the gross margin. Model cost falls as the ecosystem commoditizes; hosting scales sub-linearly; one human supervises ever-larger volumes. Margin expands as a function of engineering, not headcount.

Here is why the difficulty is worth it. A traditional services firm tops out around 30% gross margin. Pure software carries higher margin but often a smaller addressable market. The bet of the AI-native service company — and bet is the honest word, since these figures come from people with reasons to be optimistic about the thesis — is that operating leverage pulls it toward software-like margins, 50% and up, on a market perhaps two to three times larger than software, because it is addressing the labor budget rather than the tooling budget. You do not need to be there on day one. The trajectory simply has to be believable, and every line of product you ship should bend it the right way. This is the Human FTE versus Digital FTE economics stated as an income statement: a worker that runs 168 hours a week at a fraction of human cost is not only a productivity story, it is a margin story — and the P&L is where the margin story becomes real.

11. Staying on the Right Side of the Line

Everything above describes how these companies win. Intellectual honesty — the kind this book has insisted on since its preface — requires the other half.

Most of these companies will fail, and the ways they fail are predictable. They ship slop and call it a product. They skip the eval suite because reading traces is tedious, and they never learn their Digital FTE is wrong until a customer does. They fake the closed loop with a dashboard that looks like feedback but changes nothing. They let the forward-deployed motion curdle into consulting because the product engine was never really there. Or they pick a wedge with no real pain and discover that "would be nice" does not survive a renewal conversation.

There is a survivorship trap in every chapter like this one, this one included. The winners are visible because they are loud; the majority who quietly abandoned their AI initiatives are invisible because failure does not issue press releases. The lectures and founder threads that inspired this material are, in the end, encouragements delivered to rooms full of people about to try. Read them as fuel, not as forecast.

The same skepticism belongs on the productivity numbers you will be tempted to quote. When Garry Tan claims he is hundreds of times more productive than he was a decade ago, he footnotes it carefully — the figure is measured in logical code change rather than raw lines, which AI inflates, across his own repositories, with AI writing most of it. Cite it as an illustration of a genuine shift, not as a law of nature.

The deepest line is accountability, which is why a founding chapter's risk section circles back to the idea of the right side of the line. A founder owns every outcome their Digital FTEs produce, and in regulated wedges that ownership is the entire game. Salient is not built with compliance added afterward; it is built compliance-first, with real-time monitoring against the alphabet of consumer-lending regulation — CFPB, FCRA, TILA, UDAAP, TCPA. In those markets, compliance is not a feature you bolt on after product-market fit. It is the wedge, and the founder who treats the rules as the moat rather than the obstacle is the one standing on the right side of the line.

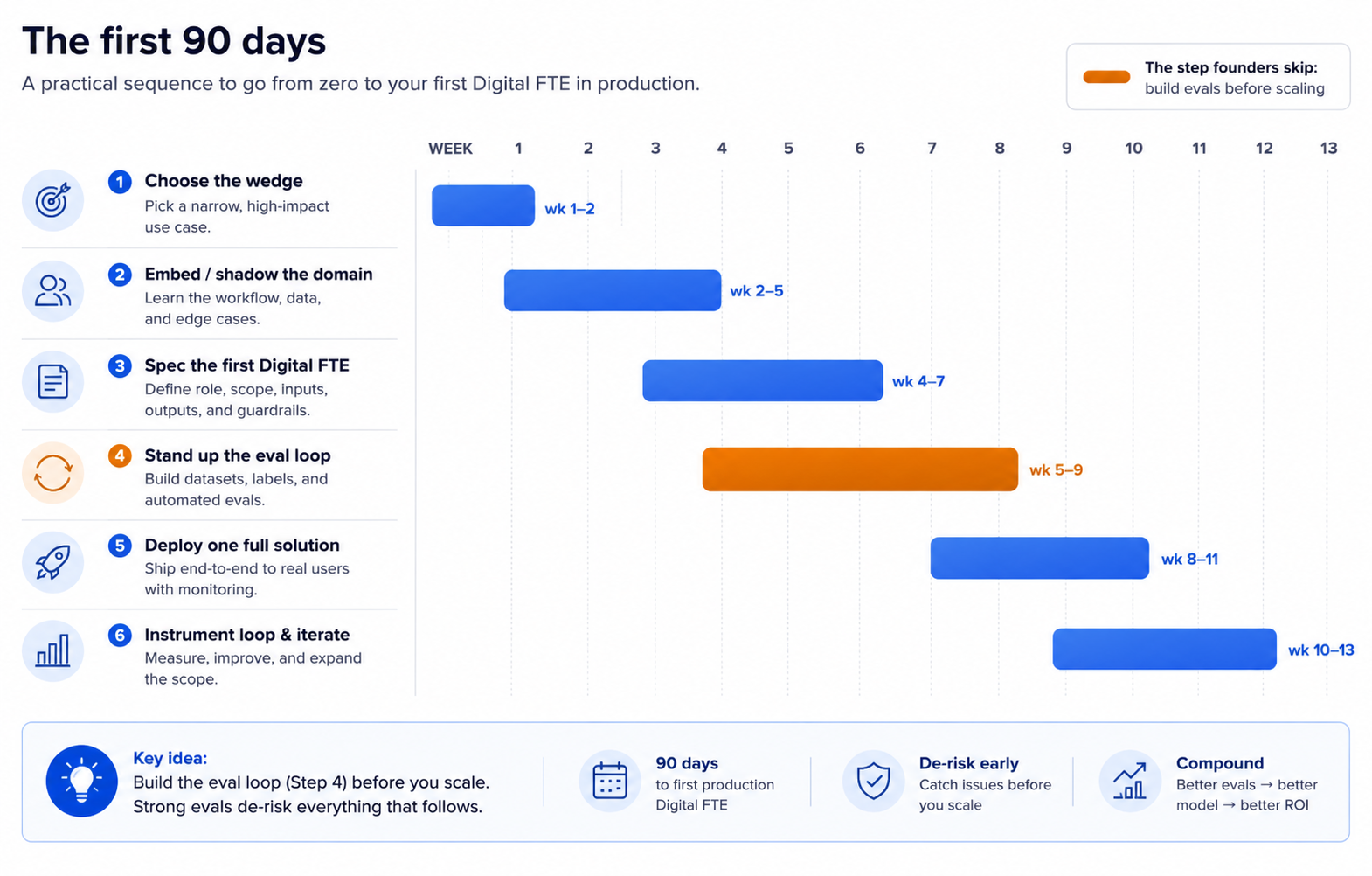

12. The First 90 Days

If you want a place to begin on Monday, here is the sequence. It is deliberately concrete.

The phases overlap on purpose. Note that the eval loop is stood up before scaling, not after.

The phases overlap on purpose. Note that the eval loop is stood up before scaling, not after.

Weeks 1–2 — Choose the wedge. Find one painful workflow that fails the three tests only by being too painful to ignore. Resist the urge to pick a category.

Weeks 2–5 — Embed. Go into the domain. Shadow the people who do the work. Learn what is not in the training set — the edge cases, the unwritten rules, the reason it is still done by phone.

Weeks 4–7 — Spec the first Digital FTE. Use the Agent Factory. Write the specification before you write the agent, and define the single outcome it owns.

Weeks 5–9 — Stand up the eval loop first. Before scaling anything, build the harness that tells you when the worker is wrong. This is the step the failures skip.

Weeks 8–11 — Deploy one full solution to one customer. Run the narrow pilot: one portfolio, one agent, clear guardrails, a measurable outcome in weeks.

Weeks 10–13 — Instrument the closed loop and iterate on traces. Read what the worker actually did, label it, feed it back, sharpen the evals. This is the work, and it does not end.

Ongoing — Price against headcount, watch the three COGS lines (model, hosting, humans) from the first invoice, and expand inside the customer before widening across customers.

The arc of this book runs from a one-person frontier lab to a manufactured, supervised workforce. This chapter is where that lab becomes a company — not a metaphor and not a deck, but a closed-loop AI-Native Company that a single founder can stand up and a small Edge Layer can run. The window is open and the map still has white space on it.

Flashcards Study Aid

Test Your Understanding

Sources and Further Reading

The factual claims, figures, and named examples in this chapter are drawn from public reporting and primary sources current as of early 2026. Funding figures, revenue, and company details change quickly; verify specifics before publication, and treat market-size projections, margin targets, and self-reported productivity multiples as estimates and goals from interested parties.

- Anthropic Economic Index — task coverage by occupation, augmentation versus automation, and the unevenness of adoption. (anthropic.com/research)

- Jack Dorsey & Roelof Botha, From Hierarchy to Intelligence (2026) — the company-as-intelligence model, the three-role org, the "humans at the edge" framing, and Block's 2026 restructuring.

- a16z, The Palantirization of Everything (2026) — the forward-deployed engineer model and the conditions under which it breaks down.

- OpenAI, OpenAI launches the OpenAI Deployment Company (May 2026), and Anthropic's parallel forward-deployed engineering venture — the frontier labs formalizing the embedded-FDE model at scale.

- Y Combinator (Charlie Warren, Visiting Partner), How to Build an AI Services Company — youtube.com/watch?v=gSNFJbgoaHI. The four traits of a great service market, the Sam Altman test, the operations mindset, variance as the existential problem, the early demand trap, per-unit and outcome pricing, the COGS and AI-operating-leverage walkthrough, and the build-versus-buy rule.

- Panacea (ycombinator.com/companies/panacea) — AI-native FDA regulatory services; the consultants-paired-with-platform model and outcome/milestone-based pricing.

- General Legal (ycombinator.com/companies/general-legal; Law.com; Artificial Lawyer) — the AI-native law firm built by the Casetext team (founders ex-Casetext, Fenwick, and Cooley); flat-fee-per-contract pricing, shift-work throughput, and sub-hour turnaround.

- Salient (trysalient.com; Crunchbase; Fortune; the Consumer Portfolio Services deployment announcement) — loan-servicing voice agents, revenue, team size, compliance posture, and pilot motion.

- HappyRobot (happyrobot.ai; Reuters; FreightWaves; Tech.eu) — freight automation, funding, customer roster, forward-deployed team, and the verticalization thesis.

- Reducto (reducto.ai; PRNewswire; Fortune) — the document-intelligence layer, funding, processing scale, and lean team.

- Garry Tan / Y Combinator (the Lightcone podcast; public statements on evals as moat; the gstack repository and its productivity-measurement caveats).

- Gartner, Over 40% of Agentic AI Projects Will Be Canceled by End of 2027 (June 2025) — the project-cancellation forecast; cited as a forecast, not a measured outcome.

The Service-as-Software repricing and the Human-FTE-versus-Digital-FTE economics are developed in The AI-Native Transformation; the maturity ladder, the spec-driven foundation, the Two-Layer Model, the Digital FTE, and the Seven Invariants are developed in The Agent Factory Thesis and across this book.