AI-Native 财务目录:AI 公司的定价、预测与财务架构

如果你刚接触这一切,请从这里开始

这是一份很长的文档。你不需要读完整篇才能开始使用。如果你刚接触财务,或者正在经营一家早期 AI 公司,下面就是对「我该做什么?」这个问题最简单的答案。

本周。 配好 Stripe(或同类工具)来处理计费。把它接到一个简单的记账工具上,例如 Pilot、Bench、Puzzle、Mercury Treasury,或任何能自动化基础工作的类似工具。从现在开始追踪三个数字:收入、毛利率(收入减去算力成本以及其他按使用量计费的供应商成本)和以月为单位的现金 runway。

本月。 建一个简单的电子表格,按月列出未来 18 个月,并向前预测同样三个数字。每个月第一个工作日更新一次。每月比较实际值和预测值。差异就是你理解业务真实运转方式的入口。

本季度。 有了三个月收入数据后,看平均毛利率。如果低于 50%,你的单位经济很可能已经失衡。多数 AI-native 业务需要 60%+ 的毛利率才能在规模化后活下来,而 SaaS 常规预期是 75–85%。低于 50% 是一个信号,说明要检查算力成本、供应商定价,或者你的定价模型是否适配成本结构。

今年。 不要雇 CFO。不要雇会计团队。不要购买企业级 FP&A 软件。除非投资人明确要求,否则不要做审计。把省下的时间用来增长收入,因为大多数财务工作只有在你已经有值得管理的实质性收入后才真正重要。

这就是 AI-native 公司前 12 个月的完整处方:Stripe + 一个记账工具 + 三个数字 + 一张简单的预测表。本文其余部分是为你超出这套配置之后准备的:当收入模型足够复杂、投资人要求足够高,或团队规模大到简单 stack 无法继续扩张时,再使用它。

如果你想在回到上面的处方前先看一个稍宽的概览,下面的「初学者 10 分钟版本」会给出更大的地图。

初学者如何阅读这份文档

如果你是真正的初学者,不要线性阅读本文。这个目录面向很多读者:创始人、CFO、controller、投资人;其中大部分内容暂时还不属于你。按顺序阅读下面五节;在你有真实收入之前,其他内容都可以先跳过:

- 如果你刚接触这一切,请从这里开始(上文):第一年的直接处方。

- 初学者 10 分钟版本(下文):更大的图景:四个家族、十二种 approach,每种用一句话说明。

- Approach 2 — Per-Call / Usage Pricing(Section A):最常见的 AI 定价模型,也是你最可能先运行的模型。

- Approach 7 — Compute COGS Accounting(Section B):每位创始人都必须理解 AI 业务毛利率的地方。

- Appendix A — Glossary(文末):遇到陌生术语时打开它。

这就是完整的 beginner reading path。五节加起来大约 4000 words。在你有具体问题前,可以跳过 executive summary、finance diagnostic、strategic fit matrix、另外十种 approach、cross-cutting concepts、AI-era shifts、common failures 和 anti-patterns。

当你已经有实质性收入后(通常是 $1M+ ARR),再回到本文,并按任何你感兴趣的顺序阅读其余部分。

这份文档放在哪里

这份文档属于 《AI-Native Company》系列。《Agent Factory 论纲》 定义架构。《AI Worker 目录》 定义要构建什么。《销售目录》 和 《营销目录》 讲公司如何销售并创造需求。Finance Catalog 定义公司如何记账、给产品定价、预测未来,并向资助它的人报告。

本文回答的是一个运营问题:考虑到成本结构、定价模型和预测问题都与传统 SaaS 有显著差异,AI-native 公司到底该如何运行财务侧?

你可以单独阅读本文。文中少量指向 Sales Catalog 的交叉引用(其中介绍了 pricing motions)即使跳过,也不会影响主线论证。

如何阅读这份文档

这份文档是一件工具,不是一个故事。不同读者会以不同方式使用它。

如果你刚接触财务。 按上面的「初学者如何阅读这份文档」阅读。第一次不要试图读完整个目录,其中大部分内容暂时还不属于你。

如果你是正在经营早期 AI 公司的创始人。 使用下面的 Finance Diagnostic 和 Strategic Fit Matrix,找出哪些 pricing architectures 适合你的买方和阶段。阅读 Section A 中相关的 approaches。在你有值得预测的收入之前,先跳过更深的会计和预测章节。

如果你是 AI 公司的 CFO、controller 或 finance lead。 这份文档就是为你设计的。请从头读到尾。各 approach 的顺序从 pricing(最常见的入口)开始,经过 accounting mechanics、forecasting,最后到 external reporting。

如果你是投资人或董事会成员。 Investor & Board Reporting approach(Section D)以及文末附近的 Common finance failures 最直接相关。

关于术语的一点说明。 本文会使用 accounting、FP&A 和 SaaS finance 中的技术词汇。专业术语第一次出现时,通常会在附近用普通语言解释。Appendix A: Glossary 提供快速参考。下面的「你必须先了解的财务术语」会覆盖你最常遇到的十五个重要术语。

关于专业建议的说明。 本文提供战略框架和运营参考,不构成专业会计、税务、法律或财务建议。ASC 606 下的收入确认、训练成本资本化、审计处理、销售税和公司结构问题,都需要合格专业人士结合你的具体情况给出建议。重大决策请聘请合格专业人士;本目录是对话起点,不是替代品。

关于置信度标注的说明。 文中一些 benchmark claims 和数值范围会带有标签,用来提示读者对具体数字应有多大信心。[Industry benchmark] 代表从业者广泛共识,并在 SaaS finance 文献中被反复引用(LTV/CAC > 3;成熟 SaaS 毛利率 75–85%;Burn Multiple 低于 1.5× 是健康 SaaS 标准)。[Emerging pattern] 代表 2024–2026 年在多家 AI-native 公司中观察到的模式,但还没有被规范参考资料完全固化(AI-native 毛利率 50–70%;compute 占收入 20–60%;foundation-model 价格每年下降 30–60%)。[Author thesis] 代表基于观察模式做出的推断,读者应把它视为一种观点,而不是定论(worker cards 中的特定 cost-per-outcome 范围、各阶段员工生产率 benchmark、按 modality 划分的 compute cost 范围)。未标注的数值主张位于这个谱系中的某处;标注是选择性的,不是穷尽性的。

初学者 10 分钟版本

如果你只有十分钟,就读这一节。它会让你理解 AI-native 公司如何处理财务,而不需要进入本文其余部分的深度。

什么是「AI-native finance」,它和普通 SaaS finance 有什么不同?

AI-native finance 是为使用基础模型、AI agent 或其他 compute-intensive AI workloads 的公司进行定价、会计、预测和报告的实践。它和传统 SaaS finance 有三个重要区别。第一,成本结构:传统 SaaS 因为托管成本相对收入很小,毛利率通常有 75–85% [Industry benchmark];AI-native 公司通常只有 50–70% 毛利率,因为 compute 是成本中的重要部分 [Emerging pattern]。第二,定价模型:传统 SaaS 卖 per-seat subscriptions;AI-native 公司经常使用 per-call、per-token、per-outcome 或 hybrid pricing,因为服务成本会随使用量变化。第三,预测复杂度:传统 SaaS 预测可以假设单位成本稳定;AI-native 预测必须考虑 foundation-model 价格每年下降 30–60% [Emerging pattern]、由使用量而不是 seat 驱动的客户 ramp curves,以及会以不同方式确认收入的合同结构。

财务 approaches 的四个家族

本文把十二种 approach 分成四个家族:

- Pricing architectures(1–5)。 AI 公司如何向客户收费。例子包括 per-seat(传统)、per-call(AI infrastructure 标准)、per-outcome(service-as-software)、value-based(按已衡量客户价值的一定比例收费)或 hybrid combinations。

- Revenue & cost mechanics(6–8)。 AI 公司如何核算收入和支出。例子包括 usage-based contracts 的 revenue recognition、compute COGS 处理、带 model-cost decay 的 cohort analysis。

- Planning & capital allocation(9–11)。 AI 公司如何预测和预算。例子包括 pilot-economics modeling、在 compute costs 下降背景下的收入预测,以及 compute 和 people 之间的资本分配。

- External reporting(12)。 AI 公司如何与投资人、董事会和审计师沟通。例子包括 investor metrics、board dashboards 和 audit-defensible disclosures。

十二种 approach,各用一句话概括

- Per-Seat Pricing。 按每位用户收取固定月费;它来自传统 SaaS,但对 compute costs 可变的 AI 产品越来越不合适。

- Per-Call / Usage Pricing。 按 API call、token 或 query 收费;这是 AI infrastructure 的主导定价模型,也是 AI 产品最常见的起点。

- Per-Outcome Pricing。 只有当 AI 交付一个定义明确的结果时才收费:一个 resolved support ticket、一笔 processed claim、一次 booked meeting。

- Value-Based Pricing。 按已衡量客户价值的一定比例收费;只适合有成熟买方的战略性 enterprise deals。

- Hybrid Pricing。 组合多种架构:base subscription 加 usage overages,或 subscription 加 outcome bonuses。

- Revenue Recognition for AI Contracts。 决定收入何时进入账本的会计规则(ASC 606);usage-based 和 outcome-based contracts 会让它更复杂。

- Compute COGS Accounting。 在 income statement 上如何处理 foundation-model API calls、GPU rentals 和 infrastructure compute 的成本。

- Cohort Analysis with Model-Cost Decay。 随着 foundation-model costs 下降,追踪 customer cohorts 如何随时间变得更赚钱。

- Pilot Economics & Contract Mechanics。 核算 paid pilots、扩张到 production contracts,以及多数 enterprise AI deals 所使用的多阶段商业结构。

- Revenue Forecasting Under Falling Compute Costs。 构建 12–24 个月收入和毛利率预测,并明确建模每年 30–60% 的 compute price reductions。

- Capital Allocation。 决定 incremental dollars 如何在 compute、people、marketing 和 runway 之间分配。

- Investor & Board Reporting。 设计 AI-native 投资人和董事会期待的 metrics、dashboards 和 disclosures;这些与传统 SaaS norms 有明显不同。

每种 approach 的初学难度

- Easy(直观、常见起点):Per-Seat Pricing(1)、Per-Call Pricing(2)

- Medium(需要运营纪律):Per-Outcome Pricing(3)、Hybrid Pricing(5)、Revenue Recognition(6)、Compute COGS(7)、Pilot Economics(9)、Capital Allocation(11)、Investor Reporting(12)

- Advanced(需要成熟财务职能或外部顾问):Value-Based Pricing(4)、Cohort Analysis(8)、Forecasting Under Falling Costs(10)

这就是十分钟内能读完的整份文档。其余部分会详细解释每一块,并给你工具来选择、排序和运行自己 AI 公司的财务架构。

你必须先了解的财务术语

如果财务对你还很陌生,下面是本文最常出现的十五个术语。理解它们后,你就能阅读后文而不必频繁查术语表。(文末 Appendix A 中有覆盖本目录 50 多个术语的完整 glossary。)

Revenue。 公司从客户那里赚到的钱。它是 income statement 的 top line。

Bookings。 某一时期内签下 deals 的总合同价值。它不同于 revenue:一份 $1.2M 的一年期合同在签署当天是 $1.2M bookings,但会在合同期内每月产生 $100K revenue。

Recognized revenue。 在 GAAP 规则下,某一期间进入 income statement 的合同收入部分。对传统 subscription contracts,recognized revenue 是 bookings 除以合同期限;对 AI-native 的 usage-based 和 outcome-based contracts,两者会明显分离。

ARR(Annual Recurring Revenue)。 subscription customers 的年化合同价值。它是最常被追踪的 SaaS 指标。一个按 annual contract 每月支付 $10K 的客户,会贡献 $120K ARR。

COGS(Cost of Goods Sold)。 向客户交付产品的直接成本。对 AI-native 公司,COGS 包括 foundation-model API costs、hosting 和 infrastructure,以及交付服务所需的可变 customer-success 时间。Compute 通常是最大的 line item。

Gross margin。 Revenue 减去 COGS,并以收入百分比表示。它是最重要的盈利能力指标。传统 SaaS norms 是 75–85%;AI-native norms 是 50–70%,因为 compute 是成本中的重要部分。

NRR(Net Revenue Retention)。 来自 existing customers 的 recurring revenue 保留比例,包含 upsell。高于 100% 表示现有客户群的收入在增长。130% NRR 意味着一年前同一批客户贡献的 $1M revenue,现在变成 $1.3M。

CAC(Customer Acquisition Cost)。 获取一个新客户的 fully-loaded cost,包括 sales spend、marketing spend,以及任何参与获客的其他职能成本。

LTV(Lifetime Value)。 一个客户在其整个客户生命周期中预计贡献的总 gross-margin contribution。

LTV/CAC ratio。 Lifetime value 除以 acquisition cost。健康 SaaS programs 的目标通常高于 3×。

CAC payback period。 客户的 gross-margin contribution 偿还获客成本所需的月份数。成熟 SaaS 的目标通常低于 18 个月。

Cash runway。 公司按当前 burn rate 维持运营、直到现金耗尽前还能撑多少个月。这是早期公司最基础的财务指标。

Burn rate。 公司每月流出的净现金,通常是 operating expenses 减去 collected revenue。一家公司每月支出 $500K、收款 $200K,则 burn rate 是 $300K/month。

Burn Multiple。 同一时期内 cash burned 除以 net new ARR added。越低越好;AI-native 低于 2× 属于健康,成熟 SaaS 低于 1.5× 属于健康。该指标由 David Sacks 推广。

Compute COGS。 运行 AI workloads 的成本:foundation-model API calls、GPU inference、infrastructure compute。在 AI-native 公司中,它作为 COGS 中的核心 line 处理,通常占收入 20–60%。

ASC 606。 美国收入确认会计准则。它决定收入何时进入账本,对有 usage-based 和 outcome-based contracts 的 AI-native 公司尤其重要。国际等价准则是 IFRS 15。

这十五个术语会在本文中出现数百次。其他词汇(variable consideration、deferred revenue、contribution margin、capital efficiency ratio、Rule of 40、audit defensibility)都建立在它们之上。如果你理解了上面的十五个,就能读懂本文其余部分。

AI-native 公司最少要追踪的财务指标

如果你只追踪十个指标,就追踪这些。下表是一家任意阶段 AI-native 公司最简单的 scorecard:它列出决定业务是否可行的指标、计算公式,以及你应当瞄准的目标。Section E 和 Section F 会给出完整指标集;这张表是地板,不是天花板。

| # | Metric | Formula | Why it matters | Target |

|---|---|---|---|---|

| 1 | Revenue(已确认) | 按 GAAP 规则在该期间赚取的 revenue 总和 | top line;income statement 报告的内容 | 月环比增长 |

| 2 | ARR | subscription contracts 的 annualized recurring revenue | 标准 SaaS scale metric | 取决于阶段 |

| 3 | Gross margin | (Revenue − COGS) / Revenue | unit economics 是否成立 | AI-native 为 50–70%,成熟 SaaS 为 75–85% |

| 4 | Compute as % of revenue | Compute COGS / Revenue | AI 特有的成本比例 | scaling stage 为 20–35% |

| 5 | Cash on hand | 期末 liquid cash 总额 | 生存指标 | 至少 18 个月 runway |

| 6 | Monthly burn | Operating expenses − revenue collected | 现金流出速度 | 取决于阶段 |

| 7 | Cash runway | Cash on hand / Monthly burn | 还能支撑多久 | 18+ 个月 |

| 8 | NRR | (Starting ARR + Expansion − Churn − Contraction) / Starting ARR | existing customer health | >110% 健康,>130% 强 |

| 9 | CAC payback period | CAC / (Monthly recurring revenue per customer × Gross margin) | acquisition 多久回本 | <18 months |

| 10 | Burn Multiple | Net cash burned / Net new ARR added | growth phase 的 capital efficiency | AI-native <2×,成熟 SaaS <1.5× |

每周追踪 cash 和 runway;每月追踪 revenue、ARR、gross margin、compute %、NRR 和 burn;每季度追踪 CAC payback 和 Burn Multiple。从你的记账工具中更新这些指标;不要维护一张和账本背离的 spreadsheet。

如果你持续追踪这十个指标,就具备了判断业务是否健康的运营纪律,也具备了和投资人对话的可信度。本文其他内容都是补充深度。

执行摘要

AI-Native Finance Catalog 是一本 recipe book,用于处理 2026 年及以后 AI-native 公司的财务侧。AI 业务有很多种定价、核算、预测和报告方式;正确方式取决于你的买方、阶段、合同结构和投资人预期。本文命名十二种 approach,把它们组织成四个家族,并告诉你哪些适合你的情况。

四个家族:每类 approach 的用途。

Pricing architectures(Approaches 1–5)定义公司如何向客户收费。这个选择会层层影响其他一切:revenue recognition、forecast complexity、sales-team compensation、customer-success focus。多数公司从一种 architecture 开始,并在规模化过程中演化为 hybrid。

Revenue & cost mechanics(Approaches 6–8)定义公司如何核算赚到的钱和花出去的钱。财务的技术工作在这里:把客户活动转成可审计的账本,正确分类 compute costs,并保持 cohort discipline,让 unit-economics truth 浮出水面。

Planning & capital allocation(Approaches 9–11)定义公司如何向前看。预测 AI 业务不仅要建模 revenue ramp,还要建模不断下降的 compute costs、扩张中的 usage,以及 AI capability 变化所带来的 customer behavior changes。Capital allocation 决定 dollars 如何在公司的三大成本中心之间分配:compute、people 和 customer acquisition。

External reporting(Approach 12)定义公司如何与投资人、董事会和审计师沟通。AI-native 公司会报告传统 SaaS 不需要的 metrics:model cost as percentage of revenue、gross margin including compute、contribution margin per outcome,以及按 model-price decay 调整后的 forecast accuracy。

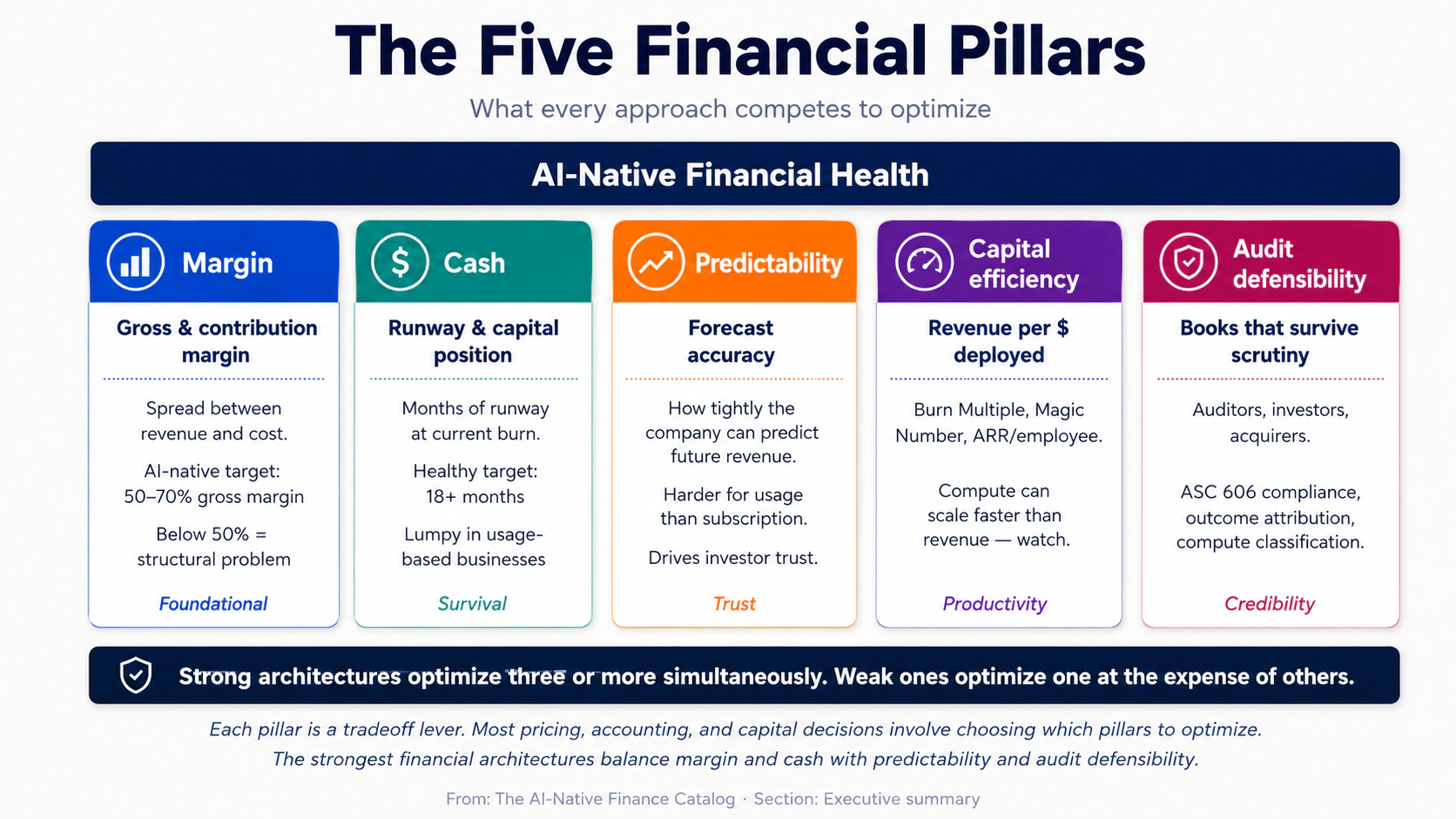

五个财务支柱:每种 approach 都在竞争优化什么。

Margin 是 revenue 和 cost 之间的差。Gross margin(收入减去 compute 和 direct costs)决定业务模型是否成立。AI-native 公司如果上线时毛利率低于 50%,很少能恢复;高于 70% 的公司则拥有实质 pricing power。

Cash 是决定 runway 的指标:公司有多少资本,以及按当前 burn rate 能撑多久。AI-native 公司经常出现 lumpy cash flows,因为 usage-based revenue 会随客户活动突然上升或收缩,也因为对 foundation-model providers 的 prepaid compute commitments。

Predictability 是预测准确度。传统 SaaS 因为 subscription revenue 可预测,所以能达到较高 forecast accuracy;AI-native 业务面临结构性 forecast uncertainty,来自 usage variance、model-price decay 和 outcome-attribution complexity。

Capital efficiency 是每投入一美元资本产生多少收入。Burn Multiple(burned capital 除以 net new ARR)和 Magic Number(sales efficiency)是常见 shorthand。AI-native 公司面临特别的效率挑战,因为 compute spend 可能比 revenue 更快扩张。

Audit defensibility 是账本经受审查的能力,包括年终审计中的 auditors、diligence 中的 investors,以及 M&A 中的 acquirers。AI-native 公司围绕 outcome attribution、usage-based revenue recognition,以及 model fine-tuning costs 的资本化还是费用化处理,面临新的 audit-defensibility 挑战。

最强的财务架构会同时优化三个或更多支柱。最弱的架构只优化一个支柱(通常是 margin 或 cash),并牺牲其他支柱;这会带来短期胜利和长期崩塌。

范围说明。 本目录主要关注从 seed 到 Series C 任意阶段的 B2B AI-native 公司。Consumer AI companies(拥有数百万免费用户、通过 tiered subscriptions 或 ads 变现的应用)遵循不同规则,不是本文的主要对象;不过 Per-Seat Pricing、Per-Call Pricing 和 Hybrid Pricing 等若干 approach 同时适用于两种语境。Late-stage public-company finance(IPO readiness、public-company reporting、segment disclosures)也不在本文范围内。

成熟度谱系。 每种 approach 都标记为 Proven、Emerging 或 Speculative,依据是今天有多少 AI-native 公司已经成功运行它。

- Proven approaches 已有许多 at-scale companies 在运行,并有成熟 playbooks 和 benchmarks。

- Emerging approaches 已在 2026 年的 AI-native 公司中运行,但会随底层 tooling 和 accounting standards 快速演化。

- Speculative approaches 依赖尚未大规模存在的实践或买方行为。

本页用于什么

本文有三个用途。

第一,作为选择器。 正在设计 AI 公司财务架构的创始人或 finance leader,可以使用 Strategic Fit Matrix、Finance Diagnostic 和 Approach Summary Table,找出适合自身阶段、买方和合同结构的架构。

第二,作为参考。 正在运行某个现有架构的 finance team,可以用深度章节审计自己的运营,对照文中模式比较 gross margin、cohort behavior 和 forecast accuracy。

第三,作为排序指南。 多数成功的 AI-native 公司会随着规模演化财务架构。Common Hybrid Models 一节映射了最常见的演进路径。

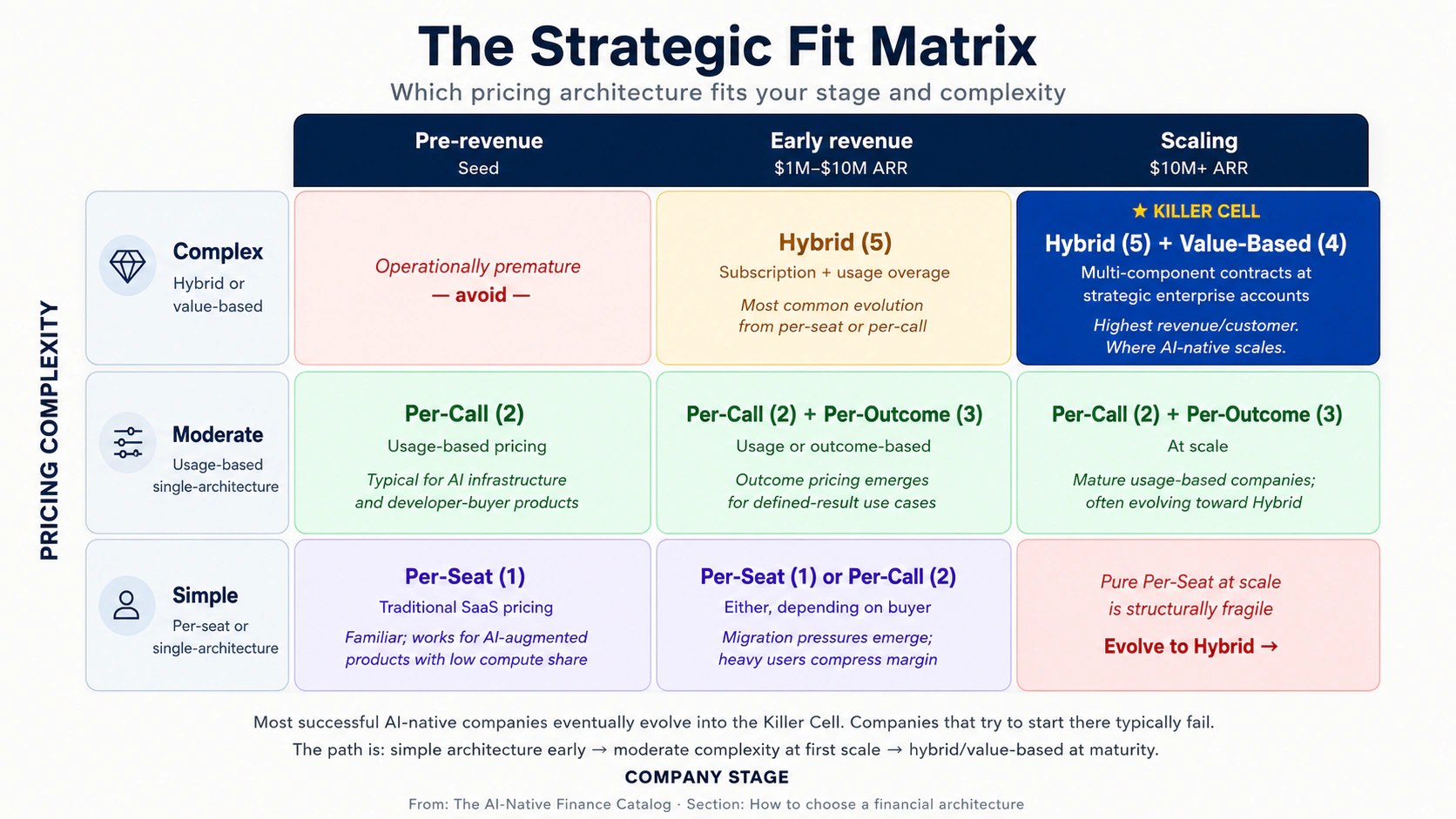

如何选择财务架构

预测哪种财务架构适合你的最干净变量,是 pricing complexity 和 company stage 的交叉点。下方矩阵把十二种 approaches 映射到这两个轴上。

| Stage → / Pricing complexity ↓ | Pre-revenue (Seed) | Early revenue ($1M–$10M ARR) | Scaling ($10M+ ARR) |

|---|---|---|---|

| Simple(per-seat 或 single-architecture) | Per-Seat (1) | Per-Seat (1), Per-Call (2) | — |

| Moderate(usage-based,single-architecture) | Per-Call (2) | Per-Call (2), Per-Outcome (3) | Per-Call (2), Per-Outcome (3) |

| Complex(hybrid 或 value-based) | — | Hybrid (5) | Hybrid (5), Value-Based (4) |

最重要的格子是 complex × scaling:Hybrid Pricing 和 Value-Based Pricing。这些架构能产生最高的 revenue per customer 和最可防守的 pricing power,但需要成熟的 finance、sales 和 customer-success operations 才能执行。多数成功的 AI-native 公司最终会演化到这个格子;试图从一开始就进入这里的公司通常会失败,因为运营成熟度尚未具备。

财务诊断:八个问题

在选择财务架构前,先诚实评估下面八个维度。每一行指向的 approaches,是与该条件最匹配的选项。

-

Buyer type。 Developer / API consumer → Per-Call (2)。Operator buying SaaS → Per-Seat (1) 或 Hybrid (5)。Enterprise buyer with budget for outcomes → Per-Outcome (3) 或 Value-Based (4)。

-

Average deal size。 <$10K/year → Per-Seat 或 Per-Call。$10K–$100K → Per-Call 或 Hybrid。$100K+ → Per-Outcome、Value-Based 或 Hybrid。

-

Cost structure variability。 Compute cost 小且稳定 → Per-Seat 没问题。Compute cost 随使用量显著变化 → 需要 Per-Call。Compute cost 很显著,但 value-per-outcome 远高于成本 → 可以考虑 Per-Outcome。

-

Sales motion。 Self-serve PLG → Per-Call 或 Per-Seat。Vendor-led mid-market → Per-Seat、Per-Call 或 Hybrid。Enterprise field → Per-Outcome、Value-Based 或 Hybrid(见 Sales Catalog Motions 7–10)。

-

Customer technical sophistication。 高(developers、technical operators)→ Per-Call 可行;用户能接受可变账单。低(executive buyers、ops)→ Per-Seat 或 Hybrid;用户想要可预测账单。

-

Contract length。 Monthly self-serve → Per-Call 或 Per-Seat。Annual SaaS → 任意 architecture。Multi-year enterprise → Hybrid 或 Value-Based。

-

Forecast accuracy required。 紧(board-driven targets、public-company-style discipline)→ Per-Seat 或 Hybrid(更可预测)。松(early-stage、growth at all costs)→ Per-Call 或 Per-Outcome。

-

Internal finance maturity。 创始人用 spreadsheet 做账 → Per-Seat 或 Per-Call(会计最简单)。已有 controller → 可以考虑 Per-Outcome。完整 finance team → Value-Based 和复杂 Hybrid 可行。

这个 diagnostic 不会告诉你哪个 architecture 绝对正确。它告诉你基于起点哪些 architecture 是可用的。上面的矩阵和下面的深度章节,会告诉你在可用架构中哪一个适合你正在定价的买方。

Approach summary table

十二种 approach 的一页参考。

| # | Approach | Maturity | Best for | Main strength | Main risk |

|---|---|---|---|---|---|

| 1 | Per-Seat Pricing | Proven | Predictable-usage SaaS | Forecast simplicity | Disconnects price from cost |

| 2 | Per-Call / Usage Pricing | Proven | Developer-buyer infrastructure | Aligns price with cost | Customer bill anxiety |

| 3 | Per-Outcome Pricing | Emerging | Defined-result use cases | Maximum value capture | Outcome-attribution complexity |

| 4 | Value-Based Pricing | Emerging | Strategic enterprise deals | Premium pricing | Contracting maturity required |

| 5 | Hybrid Pricing | Proven | Mid-market and enterprise scale | Balance of predictability and capture | Complexity to communicate |

| 6 | Revenue Recognition | Proven | Any company with revenue | Audit defensibility | ASC 606 complexity for usage/outcome |

| 7 | Compute COGS Accounting | Proven | Any AI-native company | Margin clarity | Misclassification risk |

| 8 | Cohort Analysis with Model-Cost Decay | Emerging | Companies $5M+ ARR | Truth about unit economics | Requires data discipline |

| 9 | Pilot Economics & Contract Mechanics | Proven | Enterprise sales motions | Pilot-to-production conversion | Premature production accounting |

| 10 | Forecasting Under Falling Compute Costs | Emerging | Companies on usage models | Realistic margin trajectory | Over-optimism on compute decay |

| 11 | Capital Allocation | Proven | Any post-Series A | Strategic spend discipline | Compute over-investment |

| 12 | Investor & Board Reporting | Proven | Any post-Series A | Stakeholder alignment | Vanity metrics over substance |

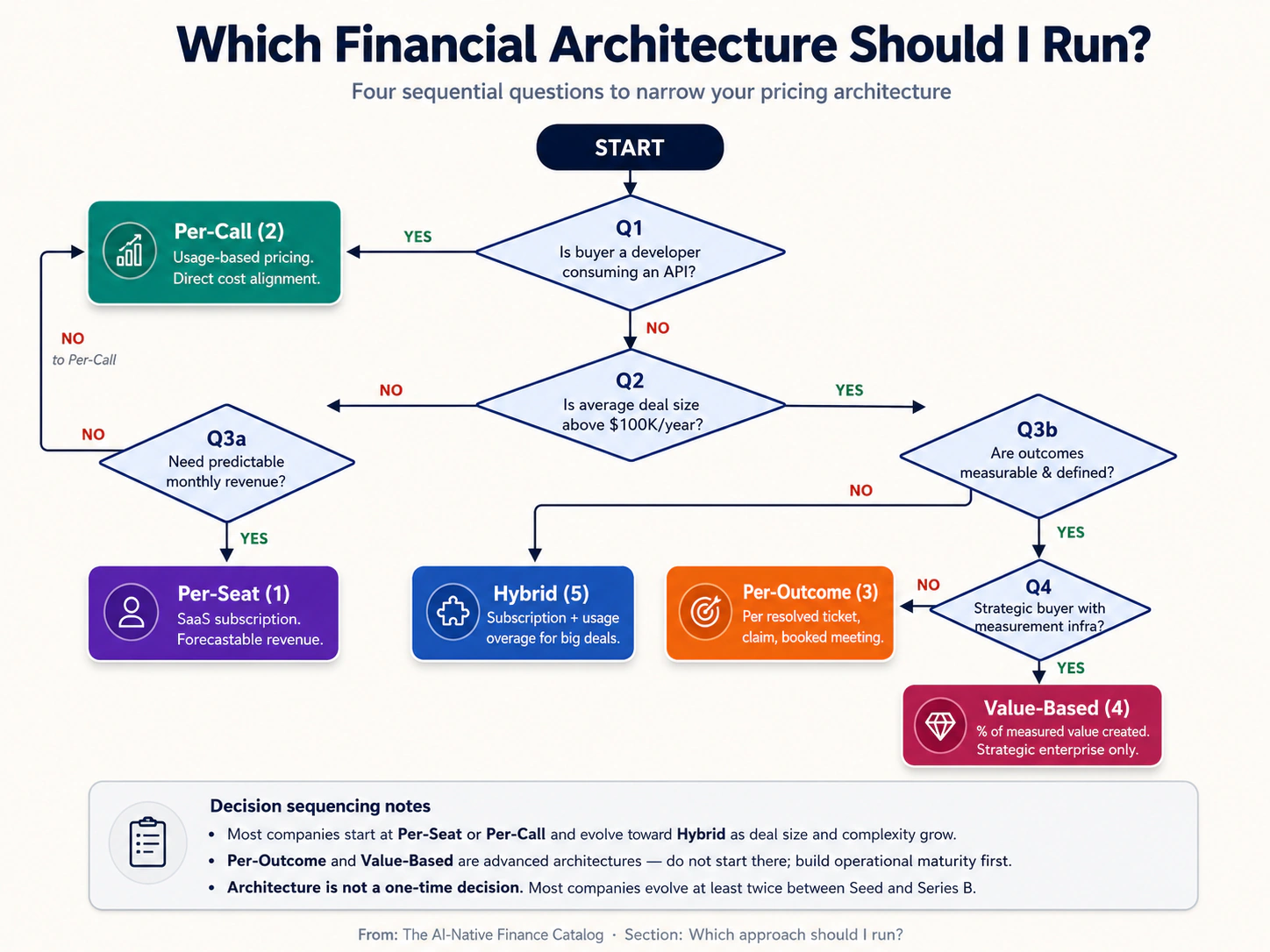

我应该运行哪种 approach?

下面的 decision flowchart 按顺序排列最重要的问题,用来缩小架构选择范围。

四个关键问题是:(1)你的买方是否是使用你 API 的 developer?(是 → Per-Call。)(2)你的 average deal size 是否高于 $100K?(是 → 考虑 Per-Outcome、Value-Based 或 Hybrid。)(3)你是否需要可预测收入来做 forecast?(是 → Per-Seat 或 Hybrid;否 → Per-Call 或 Per-Outcome。)(4)你的 finance team 的运营成熟度如何?(低 → 更简单的架构;高 → 复杂架构可行。)

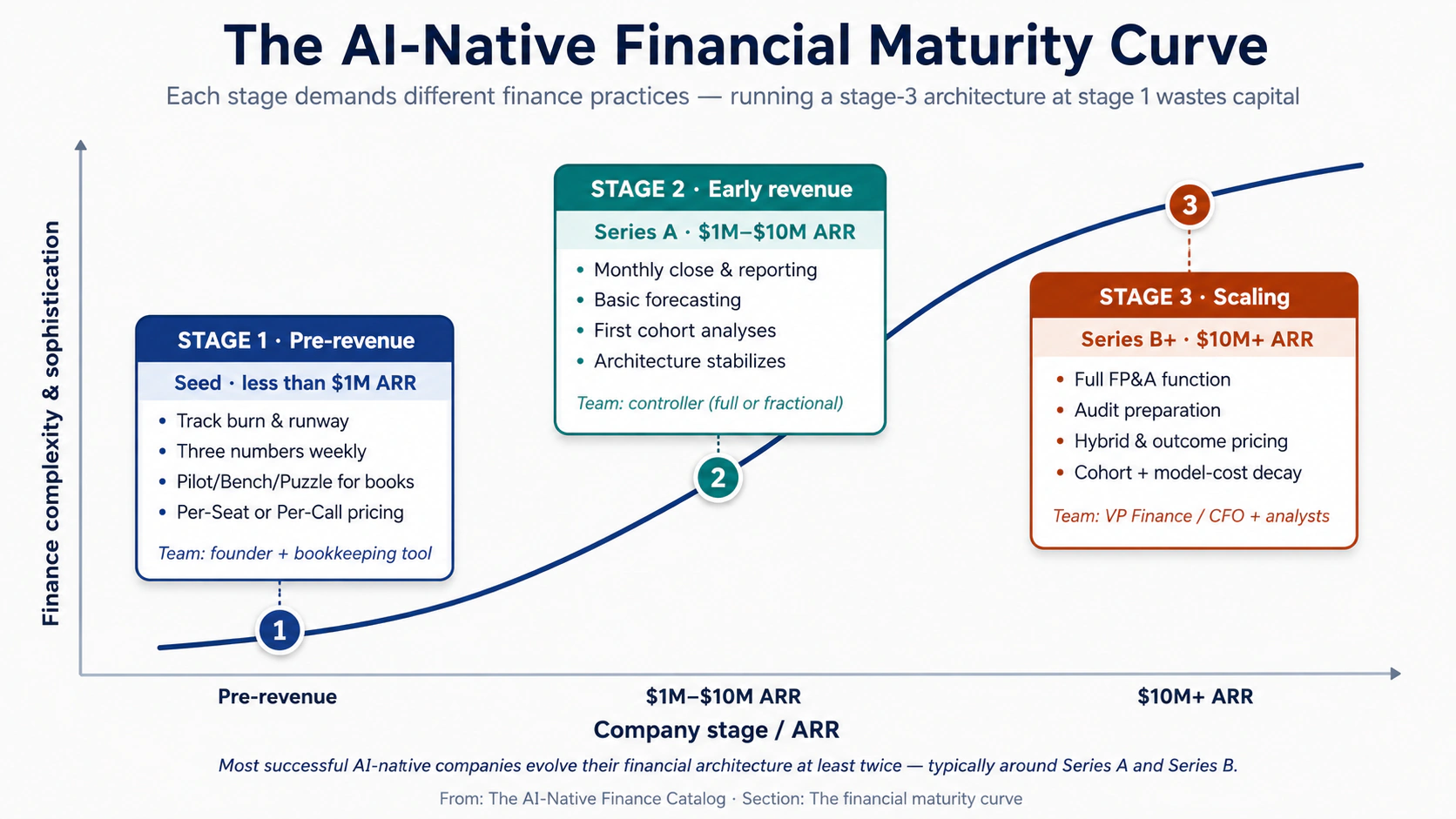

财务成熟度曲线

每家 AI-native 公司都会经历三个财务成熟度阶段。适合每个阶段的 architecture 和 operating practices 都不同,试图在 stage 1 运行 stage-3 architecture,是创始人浪费资金最常见的方式之一。

三个阶段定义了 Financial Maturity Curve:

Stage 1 — Pre-revenue(Seed-stage)。 公司有产品,但收入有限。财务工作最少:追踪 burn、管理 runway、完成基础税务申报,并为第一次 audit-equivalent 做准备(通常是 Series A diligence 期间的 Quality of Earnings review)。正确 architecture 是最容易实现、最容易向早期客户解释的 pricing model,通常是 Per-Seat(1)或 Per-Call(2)。Finance team:创始人,加上 Pilot/Bench/Puzzle 等记账工具。

Stage 2 — Early revenue($1M–$10M ARR)。 公司已有 product-market fit signals 和有意义的客户数量。财务工作扩展到 monthly close、board reporting、基础 forecasting,以及第一批内部 cohort analyses。Pricing architectures 开始稳定,但团队会看到演化压力:enterprise customers 想要不同条款,customer-success metrics 要求 outcome thinking,投资人期待更清晰的 unit economics。正确 architecture 是能够产生清晰 cohort retention,同时会计复杂度可管理的 pricing model。Finance team:controller(全职或 fractional)、bookkeeper,创始人仍参与重大决策。

Stage 3 — Scaling($10M+ ARR)。 公司正在准备或已经完成 Series B。财务工作包括完整 FP&A、audit preparation、complex contract accounting,以及越来越成熟的 investor and board reporting。Hybrid Pricing(5)和 Value-Based Pricing(4)在运营上变得可行。带 model-cost decay 的 cohort analysis(Approach 8)成为 board-level metric。Capital allocation(Approach 11)成为核心战略问题。Finance team:VP Finance 或 CFO、controller、FP&A analyst(s),以及越来越专业化的角色(revenue operations、treasury)。

对创始人的含义是,financial architecture 不是一次性决策。今天适合你阶段的 architecture,很可能在公司达到规模前至少需要演化两次:通常一次在 Series A 前后(引入更成熟的 cohort discipline),一次在 Series B 前后(引入 hybrid pricing 或 outcome-based components)。锁定 stage-1 architecture 并试图不演化就规模化的公司,通常会在 high-single-digit-millions ARR 附近遇到天花板。

成熟度图例

- Proven。 该 approach 今天已有许多 AI-native(以及 pre-AI)公司在规模化运行,并有成熟 playbooks 和 benchmarks。

- Emerging。 该 approach 正在 2026 年的 AI-native 公司中运行,但变化很快,canonical playbook 尚未稳定。

- Speculative。 该 approach 依赖尚未大规模存在的实践或买方行为。

A. 定价架构

公司向客户收费的方式。Pricing architecture 是 AI-native 公司最重要的财务决策,因为它会层层影响 revenue recognition、sales-team compensation、customer-success focus、forecast complexity 和 gross-margin structure。多数公司从一种 architecture 开始,并在规模化过程中演化为 hybrid。

Approach 1 — Per-Seat Pricing

Maturity:Proven。Beginner difficulty:Easy。

白话解释。 Per-Seat Pricing 是每个人都在 2010 年代学过的 SaaS 模型:客户按每位用户、每月支付固定费用。10 个用户,每人 $50/month,就是 $500/month。客户账单可预测,公司收入可预测,会计也直接。唯一问题是客户需要多少 seats。

对 AI 产品来说,这个模型越来越别扭。AI compute costs 随使用量扩张,而不是随 seat count 扩张。一个有 10 个 seats 的客户可能产生一万次 AI calls,也可能产生一千万次;服务成本差几个数量级,但收入完全相同。真正 AI-heavy 的产品如果采用 Per-Seat Pricing,通常会发现最重度用户贡献的是负毛利。

最适合作为 AI-augmented SaaS 的起步架构:AI 只是多个功能中的一个。对 AI 是核心价值驱动的产品,这个模型越来越不合适。

核心想法。 按用户收取可预测费用,同时接受收入不会追踪使用量,并且 heavy users 可能产生负 unit economics。

适用场景。 当产品是 AI-augmented,而不是 AI-defined,也就是 AI 是更大 workflow 产品中的一个功能。当买方是需要可预测预算 line item 的 executive。当每个 seat 的底层 compute cost 足够小(低于 subscription revenue 的 10–15%),usage variability 不会威胁 gross margin。

机制。 Per-Seat Pricing 有效,是因为它给买方和卖方都提供 predictability。买方可以做预算,卖方可以做 forecast。Annual contracts 产生 contracted ARR(annual recurring revenue),这是过去十年 Wall Street 训练 AI 公司优化的指标。

AI 产品的结构性问题,是 price 和 cost 脱节。Foundation-model API pricing 是按单位计价的:per token、per second of audio、per image generation。当产品把这个 API 包在 per-seat subscription 后面时,用户每一次调用都是卖方吸收的成本。Heavy users 往往也是客户最投入的员工,这一点有些讽刺;他们产生最多 usage,也产生最多 cost。如果所有用户平均 compute cost 是 seat revenue 的 20%,最重度的十分之一用户可能产生等于其 seat revenue 80% 甚至更高的 compute costs,留下很薄的 margin,甚至负 contribution。

2026 年的修复方式很少是彻底放弃 Per-Seat Pricing;更常见的是在合同中加入 usage-based component,也就是 included quota 以上的 per-call 或 per-token overage。这会把纯 Per-Seat 转成 Hybrid Pricing(Approach 5),而这正是规模化 AI-native SaaS 中最常见的架构。

虚构 walkthrough。 想象 MeetingMind,一款 AI meeting-summary 工具,售价 $30/seat/month。一个 100-seat 客户每年支付 $36,000。在这 100 个用户中,20 个重度使用(每人每月 50+ summaries),60 个轻度使用(5–10 summaries),20 个不活跃。20 个 heavy users 每人每月产生 $25 compute costs(合计 $6,000/year);其余用户成本很小。总 compute 大约 $7,000/year,对应 $36,000 revenue,毛利率约 80%,很舒服。现在想象随着产品粘性增强,heavy-user share 上升到 50%。Compute costs 升至 $15,000+,毛利率降到 60%。卖方要么引入 overage pricing,要么眼看 margin 被侵蚀。

Example。 Confirmed pattern:多数 AI-augmented productivity tools(Notion AI、带 AI 的 Linear、Asana Intelligence)都为核心 SaaS 采用 Per-Seat Pricing,并经常加入 usage-tier limits 来限制 compute exposure。到 2026 年,在 heavy-AI products 中很少看到没有限制的纯 Per-Seat。

Primary risk。 heavy users 带来负 unit economics。最投入的用户也是服务成本最高的用户,但他们支付的价格和轻度用户一样。Mitigation:按 user cohort 监控 compute-per-seat,一旦 heavy-user share 超过阈值就引入 usage caps 或 overage pricing,并把 Hybrid Pricing(Approach 5)视为自然演进。

First move。 计算当前客户群的 average compute cost per seat。如果它超过 seat revenue 的 15%,就开始规划向 Hybrid Pricing 迁移。

Approach 2 — Per-Call / Usage Pricing

Maturity:Proven。Beginner difficulty:Easy。

白话解释。 Per-Call Pricing 是 AI infrastructure 的标准。客户按 API call、consumed token、processed audio second、generated image 或 executed query 付费。收入随使用量扩张,成本也随使用量扩张,两者直接对齐。OpenAI、Anthropic、ElevenLabs、Replicate 以及多数 AI infrastructure companies 都使用这个模型。

优点是 gross margin 在结构上受到保护:每次 call 的收入都高于其 compute cost,因此不管客户行为如何,公司都不会在单位层面亏钱。缺点是客户账单不可预测,这会在 customer success 和 renewal 中反复制造问题:每一次 usage spike 都会带来 bill spike,超过内部预算的客户会变成不满意客户。

最适合作为 AI infrastructure products 和 developer-buyer products 的 founding architecture。在 operator-buyer products 中,也常作为 Hybrid Pricing 的一个 component。

核心想法。 让 price 直接对齐 usage 和 cost。每次 call 都让公司承担某个 compute amount,因此按高于该成本的价格收费,并内置 margin。

适用场景。 当买方是适应 usage-based billing 的 developer 或 technical user。当产品确实 usage-variable,即不同客户消耗的量差异很大。当团队愿意投入 usage instrumentation、billing infrastructure,以及帮助买方管理账单的 customer-success work。

机制。 Per-Call Pricing 有效,是因为它在 architecture 层面解决了 gross-margin 问题。每次 call 的价格都高于成本,因此 margin 在数学上受到保护。Forecasting 比 Per-Seat 更难(revenue 取决于 usage,而 usage 取决于可变的 customer behavior),但对许多 AI infrastructure products 来说,用预测难度换取 margin safety 是值得的。

执行它需要三项传统 SaaS 不需要的运营纪律。Usage instrumentation:每个可计费事件都必须被测量、归因到正确客户,并存入可审计记录。Billing infrastructure:每月生成准确、可辩护的 invoice 比固定费用计费更难,错误会立刻被客户看见。围绕 bill management 的 customer success:客户需要 dashboards 监控 usage,需要 usage spikes 时的 alerts,也需要设置 caps 或 budgets 来避免惊喜账单。没有这三项纪律就上线 usage-based pricing 的公司,会看到客户 churn 来自 bill anxiety,而不是产品不满意。

规模化后的约束是 bill-shock。一个客户一月用了 $5K compute,二月用了 $50K,就会看到 10× bill increase,需要内部批准才能付款。默认反应「我们明年再评估」会转化成收入流失。成熟 usage-based 公司会大量投入 bill-prediction tools、capacity-planning conversations,以及当 usage trajectories 暗示 budget concerns 时的主动 outreach。

虚构 walkthrough。 想象 TextAI,一家 LLM API 公司。客户按每 1K input tokens 支付 $0.005,按每 1K output tokens 支付 $0.015。典型客户注册、构建 integration,前三个月每月试验成本 $200,然后部署到 production,并在接下来的六个月 ramp 到 $5,000/month。到第九个月,客户每天处理 50M tokens,每月支付 $150K。客户账单不可预测;他们的 CFO 每月都会抱怨;customer-success team 花 30% 时间帮他们 forecast。但 TextAI 对这个客户每个月的 gross margin 都稳定在 65%,因为无论客户如何 ramp,这个 architecture 都保护业务模型。

Example。 Confirmed examples:OpenAI、Anthropic、Cohere、Mistral、ElevenLabs、Replicate、Together AI、Fireworks AI,以及 AI infrastructure companies 的长尾。2026 年几乎每家 AI-API business 都使用某种 usage pricing。

Primary risk。 Bill-shock 和 customer churn。超出预算的客户会不开心,不管产品有多好。Mitigation:投入 usage dashboards、budget alerts、与大客户每月做 capacity-planning conversations,并提供让客户设置 hard caps on spend 的选项(同时接受 hitting the cap 会造成另一种痛苦:service interruption,也需要谨慎管理)。

Secondary risk。 Forecast unpredictability。Usage-based revenue 比 subscription revenue 更难预测,会使 fundraising、board reporting 和 operational planning 更复杂。Mitigation:建立 cohort-based forecast models,用过往 customer behavior 预测 usage growth;投入 lead indicators(calls per active user、active-user growth rate),这些比 total usage 更可预测。

First move。 如果你的产品确实 usage-variable,并且买方是 technical,就从一开始上线 Per-Call Pricing。设定一个 unit consumption price,使你获得 60%+ gross margin [Emerging pattern: 低于这一 AI-native floor 后,规模化会在结构上变困难],仔细 instrument usage,并在第一个客户到来前建好 usage dashboard。

Approach 3 — Per-Outcome Pricing

Maturity:Emerging。Beginner difficulty:Medium。

白话解释。 Per-Outcome Pricing 意味着客户只在 AI 交付定义明确的结果时付费。一次 resolved support ticket、一笔 processed insurance claim、一次 booked sales meeting、一个 successful completed agent task。客户不是为 access、time 或 compute 付费,而是为 outcomes 付费。如果 AI 没有交付,客户就不付费。

这个 pricing model 有时被称为「Service-as-Software」,是过去几年 AI commercial structure 中最具辨识度的创新。它运营复杂、会计负担重,并依赖公司准确归因 outcomes 的能力。但对 outcomes 可衡量的 use cases 来说,它会产生远高于 Per-Call 或 Per-Seat alternatives 的 per-customer revenue,因为价格锚定的是客户的 labor budget,而不是 software budget。

最适合 outcomes 定义清晰、可衡量且 AI 能稳定交付的 use cases。几乎总是与 Sales Catalog Motion 9(Pay-Per-Outcome)结合。运营复杂;需要大量 outcome-attribution infrastructure。

核心想法。 按 delivered outcome 收费,把价格锚定在客户的 labor cost 上,而不是卖方的软件成本上。

适用场景。 当 use case 有清晰、可衡量、可归因的 outcome。当客户的替代方案是雇人做同样工作(因此 comparison anchor 是 human labor cost)。当公司愿意投入 outcome-attribution infrastructure,这通常是运行该 architecture 早年里最大的一项非产品工程投入。

机制。 Per-Outcome Pricing 有效,是因为它让卖方捕获客户 labor budget 的一部分,而不是 software budget 的一部分。一家 mid-market 公司花在 customer-support headcount 上的钱,可能是 customer-support software 的十倍。通过 outcome pricing 捕获一部分 headcount budget 的 AI vendor,与只捕获一部分 software budget 的 vendor 不在同一个 revenue category。

定价数学锚定在人力成本上。如果一位 customer-support representative 解决一张 ticket 的 all-in cost 大约是 $5(salary、benefits、management overhead、workspace),outcome price ceiling 大约在每张 resolved ticket $1–3:足够低于人力成本,让客户获得真实节省;也足够高于卖方 compute cost,让 gross margin 为正。卖方每个 outcome 的 compute cost(优化良好的 agent 通常为 $0.20–0.80 [Author thesis: 基于 2026 年观察到的 deployments;对 model choice 和 prompt efficiency 敏感])设定 floor;客户的人力成本设定 ceiling;price 位于两者之间。

技术基础是 outcome attribution。Vendor 必须生成 audit-grade telemetry:对每个 priced outcome,都有可验证记录说明 AI 做了什么、处理了什么,以及结果如何被确认。没有这些,客户争议就没有客观依据,revenue collection 会变成季度性谈判。运行这个 architecture 很好的公司会把 outcome-attribution infrastructure 当成产品的一部分,而不是 accounting overhead,并用 engineers 而不是 finance analysts 来 staffing。

会计复杂度是真实的。Revenue 是随着 outcomes delivered 而确认的(不是合同签署时确认),这意味着 contract-to-revenue conversion 不是 1:1:公司签下 $1M bookings,但 revenue 只会随着 outcomes accrue 在很多个月内逐步确认。再叠加标准 ASC 606 要求(Approach 6),会产生传统 SaaS finance 不必管理的 deferred-revenue mechanic。

虚构 walkthrough。 想象 TicketBot,一个 AI customer-support agent。TicketBot 不按 seat 或 call 向客户收费,而是在每张 support ticket 由 TicketBot 独立解决(不升级给 human)时收取 $0.50。每月有 50,000 张 tickets 的客户会收到 $25,000 monthly bill,但前提是 TicketBot 真的解决了这些 tickets。如果 TicketBot 只解决 30% incoming tickets,账单就是 $7,500。客户 CFO 喜欢这个模型;客户 procurement team 需要学习如何构造合同;TicketBot 自己的 finance team 必须投入 outcome-attribution infrastructure 来支撑每个 billable event。

Example。 Confirmed examples:Sierra 对 AI customer service 的 per-resolution pricing。Decagon 的 outcome-based contracts。EvenUp 为 personal-injury legal work 使用 per-claim pricing。这个模式是 2026 年扩张最活跃的 pricing structures 之一,并且几乎都出现在同时运行 Sales Catalog Motion 9 的公司中。

Primary risk。 Outcome-attribution disputes。如果没有 audit-grade telemetry,客户会争议什么才算「resolved」outcome,collection 会变成谈判。Mitigation:把 attribution infrastructure 作为核心 engineering function 投入。在第一份合同之前就建好 telemetry,不要事后 retrofit。

Secondary risk。 Revenue recognition complexity。ASC 606 下的 outcome contracts 需要谨慎结构化,并可能产生令人意外的 deferred-revenue patterns。Mitigation:从第一份合同开始就与有 AI 经验的 revenue accountant 合作;不要假设传统 SaaS revenue recognition rules 适用。

First move。 定义一个清晰、不含歧义、可衡量、可归因的 outcome。第一份合同保守定价(靠近你的 cost floor,而不是 value ceiling),先学习运营 mechanics。至少经历六个月 attribution disputes 后,再逐步提高 price。

Approach 4 — Value-Based Pricing

Maturity:Emerging。Beginner difficulty:Advanced。

白话解释。 Value-Based Pricing 意味着客户按 AI 为其创造的已衡量业务价值的一定比例付费。一家 hedge fund 部署 AI 工具,每年提升 trading efficiency $40M;AI vendor 的合同按 measurable improvement 的 15% 结构化,每年支付 $6M。价格不锚定在卖方成本或可比软件上,而是锚定在客户已衡量的 outcomes 上。

这是 AI 中 revenue-per-customer 最高、也最少见的 pricing model。它需要成熟的 contracting、买方处的 executive sponsorship(通常是 C-suite),以及大量 measurement infrastructure 投入来支撑 value calculation。到 2026 年,它主要出现在 financial services、大型 healthcare systems 和 consulting firms 的战略性 enterprise deployments 中,也就是那些既有 analytical sophistication 严格衡量 value,又有 procurement flexibility 结构化非标准合同的买方。

最适合 measured value 足够大、能够支撑运营 overhead 的战略性 enterprise deals。总是与 Sales Catalog Motion 10(Value-Based Engagement)结合。

核心想法。 按已衡量客户价值的一定比例收费,去除传统 vendor-buyer 对立动态:vendor 想为 access 收费,buyer 想为 results 付费。

适用场景。 当客户是成熟 enterprise,既有衡量 value 的 data infrastructure,也有结构化非标准合同的 procurement flexibility。当 deployment 会产生足够大的 measurable、attributable outcomes,以支撑运营 overhead(通常是 $5M+ annual measured value)。当买方的 executive sponsor 有权覆盖 standard procurement。

机制。 Value-Based Pricing 只有在双方能同意 value 的定义和衡量方式时才有效。合同结构比 seat、usage 或 outcome-based pricing 复杂得多。典型协议有四个组成部分。Baseline measurement period(通常是 deployment 前 30–90 天)建立没有 AI 时客户 metrics 的状态。Value-share formula 定义 vendor 捕获 measured gain 的比例,通常为 5–25%,随 deal complexity 和 buyer sophistication 而变化。Ceiling and floor 同时封顶 upside(避免 vendor 收入高到客户 executives 无法内部辩护)和 downside(避免 vendor 变成付钱让客户部署产品)。Audit rights 让 vendor 有能力验证客户在驱动 billing 的 metrics 上的报告;没有 audit rights,customer procurement 会在第一次 true-up cycle 低报 measured value。

运营约束是 contracting maturity。多数 enterprise procurement organizations 还无法规模化结构化 value-based deals;legal、finance 和 operations 都需要理解该模型并有权承诺非标准条款的代表。因此这些 deals 通常需要 C-suite 级别的 executive sponsor:只有这种 authority 才能覆盖 procurement organization 的默认回答「我们不这样结构化 deals」。没有 sponsor,proposal 会无限期卡在组织中层。

财务会计复杂度很高。Value-based contracts 的 ASC 606 revenue recognition 并不简单。Variable consideration 会被约束在公司能以 reasonable reliability 支撑的金额内,这通常意味着在建立 track record 之前,已确认收入会远低于合同 nominal upside。审计师第一年审查这些合同时通常很保守;第三年有多个期间可比数据后,通常会更宽松。

虚构 walkthrough。 想象 CashFlow,一款服务 hedge funds 的 AI 工具。一家 $50B fund 部署 CashFlow,并在 12 个月 measurement period 中,将每年 $40M trading efficiency improvement 归因于该 deployment。CashFlow 的合同按 above-baseline measurable improvement 的 15% 结构化:fund 在合同期内每年支付 $6M。这个 deal 谈了九个月,需要 fund 的 CIO 和 CFO 亲自批准,并且只有 executive sponsor 推动才通过 procurement。CashFlow 的 accounting team 第一年保守确认 $2M revenue,同时建立 audit-defensible track record;第二年,在 value calculation 已由多个 measurement cycles 确认后,确认完整 $6M revenue 才变得 defensible。

Example。 Emerging analogues:Anthropic Applied AI 与 strategic enterprise customers 的一些 engagements。Palantir 围绕 mission outcomes 结构化的一些 deployments。Financial services、healthcare 和大型 consulting firms 中前沿的 AI deployments。这个模式太年轻,还没有 canonical exemplar,但 Big Four consulting practices 已经越来越多地提供 contract templates。

Primary risk。 Contracting collapse。Deal 在组织中层卡几个月,因为 procurement 没有合同结构模板。Mitigation:在起草合同前识别并争取 executive sponsor。Sponsor 的 authority 是 unblock mechanism;没有它,无论方案多合理,deal 都不会关闭。

Secondary risk。 Audit conservatism。ASC 606 下 year-one revenue recognition 可能显著低于合同 nominal value,产生让投资人困惑的 P&L。Mitigation:在签第一份 value-based contract 前聘请有 AI 经验的 revenue accountant;围绕 bookings 以及 recognized revenue 组织 investor reporting。

First move。 不要把 Value-Based Pricing 作为第一个 architecture。先通过 Per-Call(2)、Per-Outcome(3)或 Hybrid(5)建立运营成熟度。只有当公司已有 controller、有经验的 contracts attorney,以及 target buyer 内部的 executive sponsor 后,再尝试 Value-Based。

Approach 5 — Hybrid Pricing

Maturity:Proven。Beginner difficulty:Medium。

白话解释。 Hybrid Pricing 把上面两个或更多 architectures 组合进一份合同。最常见模式是 base subscription(Per-Seat 或 platform fee)加上 included quota 以上的 usage overages:客户对正常 usage 有可预测预算,对 heavy usage 增量付费。其他 hybrids 会把 subscriptions 与 outcome-based bonuses 组合,或把 platform fees 与 per-call infrastructure charges 组合。

到 2026 年,Hybrid Pricing 是规模化 AI-native 公司的主导 architecture。纯 single-architecture pricing 越来越局限于尚未演化模型的早期公司。Hybrids 占主导的原因是,它们平衡了多种 architecture 的结构性优势:subscription 的 predictability、usage 的 cost-alignment,以及(对某些 hybrids 而言)outcome 的 value capture。

最适合作为 Per-Seat 或 Per-Call 在公司达到 mid-market 和 enterprise scale 后的自然演进。它增加运营复杂度,需要谨慎 contract design,以及 customer-success 对买方理解结构的投入。

核心想法。 组合多种架构,平衡 predictability、cost-alignment 和 value capture,达到任何单一 architecture 都无法单独实现的效果。

适用场景。 当 customer revenue 已达到一定规模,纯 per-seat 或 per-call 开始失效(heavy users 压缩 margin、light users 带来 churn risk,或 enterprise buyers 要求更成熟合同)。当团队具备设计并执行 multi-component pricing 所需的 contracting 和 operational maturity。

机制。 AI-native SaaS 中最常见的 Hybrid Pricing 结构是「Per-Seat plus Usage Overage」:客户按每 seat 每月支付固定费用,每个 seat 每月包含一定 AI calls quota,超过 quota 后按 per-call 收费。这个结构保留了买方喜欢的 Per-Seat 预算 predictability,同时保护卖方 gross margin 免受 heavy users 侵蚀。变体包括「Platform Fee plus Usage」(为使用 API 的权利支付固定费用,再按 per-call 收费)、「Subscription plus Outcome Bonus」(base subscription 加 advanced agents 的 per-outcome charges),以及「Tiered Subscription」(多个 subscription tiers,各自有不同 included quotas 和 per-call rates)。

执行它需要三项纪律。Contract design:multi-component pricing 需要严谨的法律和定价策略工作,避免客户困惑或无意的 margin leakage。Usage instrumentation:即使是 hybrid contracts,也需要干净的 usage tracking,用于 overage component 计费和预测 customer behavior。Customer education:operator 和 executive 角色的买方经常难以 forecast hybrid bills;customer-success team 必须投入大量时间帮助客户理解 projected costs。

财务会计复杂度位于 subscription 和 usage accounting 的交叉点。Subscription component 的 revenue 在合同期内按比例确认;usage component 的 revenue 随 usage 发生而确认。ASC 606 会把这些视为 separate performance obligations,因此合同必须按 relative standalone selling prices 在 components 间分配 transaction price。这不是简单练习,通常需要 revenue accountant 明确指导。

规模化后的约束是 communication complexity。无法轻松 forecast 账单的客户会焦虑;焦虑客户会 churn。成熟 hybrid-pricing 公司会投入 dashboards、projection tools 和最大化 predictability 的合同结构,例如 monthly true-up windows 而不是 continuous metering,或 quarterly commitments 并在季度末 review overage,而不是每月底 review。

虚构 walkthrough。 想象 AgentPlatform,一家 AI agent infrastructure 公司。它的 pricing 是 hybrid:客户每月支付 $5,000 platform fee(包含每月 1M agent calls),超过 quota 后每 call 支付 $0.005,采用 annual contracts 和 quarterly true-up。典型客户签下 $60K base annual contract,usage 从 signup 时每月 200K calls ramp 到第十二个月每月 5M calls。第一年结束时,客户实际 revenue contribution 是 $60K(subscription)加 $180K(36M extra calls × $0.005 的 overage)= $240K annual revenue,是 base contract 的四倍。客户账单足够可预测(会收到 quarterly true-up notices);AgentPlatform 的 gross margin 保持干净,因为 heavy usage 的价格高于 compute cost。

Example。 Confirmed examples:GitHub Copilot 的 Business 和 Enterprise tiers(带 usage components 的 subscription)、Cursor 的 enterprise plans(subscription plus token overages)、多数 mature pricing 的 enterprise AI vendors(Glean、Harvey、Sierra 在 large accounts)。Hybrid Pricing 是 2026 年 $10M+ ARR AI-native 公司中的主导 architecture。

Primary risk。 合同复杂度让客户困惑。无法轻松 forecast 账单的买方,比采用简单 pricing 的买方 churn 更高。Mitigation:投入 projection dashboards、使用 quarterly true-up windows 而不是 monthly,并让 customer-success conversations 带新客户走一遍 projected costs。

Secondary risk。 Revenue recognition complexity。Hybrid contracts 的 ASC 606 处理比纯 subscription 或纯 usage 更复杂;standalone-selling-price allocation 中的错误可能造成重大 restatements。Mitigation:在设计 pricing structure 前,聘请熟悉 multi-component AI contracts 的 revenue accountant;不要依赖标准 SaaS revenue-recognition templates。

First move。 如果你的 Per-Seat product 因 heavy users 遇到 margin compression,或 Per-Call product 因 bill anxiety 带来 customer-success burden,就设计一个 hybrid,加上缺失的 component(usage overage 或 subscription floor)。最简单的第一版 hybrid 是「当前 pricing 加一个单一 overage component」;不要第一天就设计六个 component 的合同。

B. 收入与成本机制

财务的技术工作:把 customer activity 转成 auditable books,正确分类 compute costs,并保持 cohort discipline,让 unit-economics truth 浮现。这些 approaches 没有 pricing 那么显眼,但对长期 financial health 更重要。公司可以带着不完美 pricing 生存几年;但经过第一次审计后,无法继续承受不完美的 revenue recognition 或 COGS misclassification。

⚠ 关于会计和税务建议的说明。 本节讨论 revenue recognition(ASC 606)、COGS classification、training costs capitalization、deferred revenue 和 audit defensibility。本目录提供战略框架,并指出你需要回答的问题;它不针对你的具体情况提供专业 accounting、tax 或 audit advice。审计师和 standard-setters 对 AI-native usage-based、outcome-based 和 value-based contracts 的 ASC 606 解释仍在演化。签署第一份 non-subscription contract 前、第一次 audit cycle 前,以及任何依赖下列规则的重大决策前,请聘请有 AI-native 实务经验的 CPA。

Approach 6 — Revenue Recognition for AI Contracts

Maturity:Proven。Beginner difficulty:Medium。

白话解释。 Revenue recognition 是一个会计问题:收入何时算进账本?客户签一份 $1.2M 一年期合同,每月支付 $100K;你是每月记录 $100K revenue,还是第一天记录 $1.2M,还是其他方式?答案由 ASC 606(美国)或 IFRS 15(国际)这类全球会计准则规定。对传统 SaaS,答案很直接:在合同期内按比例确认收入。对 AI-native 公司,事情会复杂:usage-based contracts、outcome-based contracts 和 value-based contracts 各有不同确认规则,而且审计师仍在随着合同结构演化解释这些规则。

把这件事做对很重要,因为它决定公司对投资人说什么、审计长什么样,以及 P&L 实际呈现什么。做错的公司会在第一次审计中面临 material restatements,在 fundraising 时出现意外 revenue holes,并损害需要多年才能修复的 investor credibility。

最适合作为每个阶段的 foundational discipline。不能无限期推迟;公司一旦有任何 revenue,ASC 606 就适用。

核心想法。 把 ASC 606 的五步框架用于 AI contracts:identify the contract、identify performance obligations、determine the transaction price、allocate the price to obligations、recognize revenue as obligations are satisfied。这些 AI contracts 经常包含 variable consideration、multiple performance obligations 和 outcome-dependent payments。

适用场景。 永远适用,从公司有任何 contracted revenue 的那一刻开始。应用复杂度会变化(Per-Seat 简单;Value-Based 复杂),但框架普遍适用。

机制。 传统 SaaS revenue recognition 简单,是因为合同通常只有一个 performance obligation(提供 software access),并在合同期内按比例交付。Revenue 等于 contract price 除以 contract length,并按月确认。ASC 606 在这里没有太多争议。

AI contracts 会以三种结构性方式把这件事复杂化。第一,variable consideration:usage-based 和 outcome-based contracts 的 transaction price 取决于 customer behavior,而它在签合同时并不知道。ASC 606 要求公司估计 variable consideration,但把估计限制在公司能以 reasonable reliability 支撑的金额内;在 track record 建立前,这通常远低于合同 nominal upside。第二,multiple performance obligations:把 subscription、usage 和 outcome bonuses 绑在一起的 hybrid contract 有三个或更多 obligations,每个都需要单独 price allocation 和单独 recognition timing。第三,outcome dependency:在纯 outcome-based contracts 中,只有 outcome delivered 并 confirmed 后才能确认收入;这可能让 contract signing 和 revenue recognition 之间出现 6–12 个月 lag。

实际含义是,AI-native 公司的 bookings(signed deals 的合同价值)和 recognized revenue(P&L 上的 GAAP revenue)会明显分离。某个季度 bookings 可能是 $5M,但 recognized revenue 只有 $1.5M,因为大部分合同是 outcome-based,收入确认被限制在保守估计内。投资人和董事会必须学会同时读两个数字;不熟悉这个 gap 的创始人经常误判公司财务状态。

虚构 walkthrough。 想象 OutcomeAI,一家 AI customer-support 公司。Q1 公司按平均 $2/resolved-ticket 签下 $4M 新 annual outcome-based contracts,预计客户群将产生约 2M tickets。ASC 606 要求只有在 outcomes delivered 时确认收入。到 Q1 结束,只有 200K tickets 被解决(deployment ramp 很慢),产生 $400K recognized revenue。公司 bookings 是 $4M;recognized revenue 是 $400K;deferred revenue(已签但尚未确认的合同)是 $3.6M。P&L 显示 $400K revenue;董事会需要看到所有三个数字:bookings、recognized revenue、deferred revenue,才能理解业务状态。只看到 $400K recognized revenue 就以为业务停滞的创始人是错的;只看到 $4M bookings 就以为公司有 $4M GAAP revenue 的创始人也错。

Example。 Confirmed pattern:每家有 non-subscription contracts 的 AI-native 公司都会遇到这种复杂度。Sierra、Decagon 和其他 outcome-priced 公司会在 investor materials 中报告明显不同的 bookings 和 recognized revenue figures。采用纯 subscription pricing(早期 Per-Seat 或 Per-Call)的公司 recognition 更简单,但在 fundraising 或 M&A 期间仍必须向审计师证明 ASC 606 compliance。

Primary risk。 过激确认,后来被审计师 restate。公司基于对 variable consideration 的乐观假设确认收入;审计师年末不同意;收入向下重述;投资人失去信心。Mitigation:在签第一份 non-subscription contract 前聘请有 AI 经验的 revenue accountant;正式记录 recognition policy;在第一次 audit cycle 期间就与审计师 review policy,而不是事后 review。

Secondary risk。 过度保守确认,隐藏增长。公司确认收入太保守,P&L 看起来比底层业务表现弱;投资人和董事会误判 trajectory。Mitigation:持续、分别报告 bookings、deferred revenue 和 recognized revenue;训练投资人和董事会成员如何同时读取三个数字。

First move。 阅读 FASB 的 ASC 606 standard(或让你的会计师 briefing)。用一页 memo 记录公司的 revenue-recognition policy。在第一次 audit cycle 前,与外部 accountant review。

Approach 7 — Compute COGS Accounting

Maturity:Proven。Beginner difficulty:Medium。

白话解释。 Compute COGS Accounting 是 AI-native 公司在 income statement 上处理 AI workloads 运行成本的方式。Foundation-model API calls、GPU rentals、inference infrastructure、fine-tuning compute 和 embedding generation,都会流入 cost of goods sold(COGS),也就是 P&L 上决定 gross margin 的 line。正确分类这些成本,是公司未来每个 margin metric 的基础。

传统 SaaS hosting costs 很小(通常是收入的 5–15%)[Industry benchmark],因此 COGS line 在概念上不那么重要。对 AI-native 公司,compute 经常是收入的 30–60% [Emerging pattern],这让 COGS 成为 income statement 上最关键的 line。分类错误——把应该费用化的资本化,或把应该资本化的费用化——会产生不反映经济现实的 gross-margin numbers。

最适合作为每个阶段的 foundational discipline。分类规则不是可选项;它影响公司报告的每一个 external metric。

核心想法。 正确区分 compute costs 应进入 cost of goods sold(降低 gross margin)还是 operating expenses(不降低 gross margin),并保持处理一致,让 margin trends 反映经济现实。

适用场景。 永远适用,从公司产生 compute costs 的那一刻开始。复杂度会随成本规模上升,但 discipline 普遍适用。

机制。 AI-native 公司的 compute costs 分为三类,各自会计处理不同。

Direct production compute:运行满足 customer requests 的 AI workloads 的成本。服务 customer queries 时的 foundation-model API calls、生成 customer outputs 时的 GPU inference、customer data 的 embedding generation。这一类明确属于 COGS:它是交付产品的成本,并且随 revenue 扩张。

Product-development compute:训练和 fine-tuning models、evaluation runs、research experiments,以及改善产品但不直接绑定 customer requests 的 infrastructure work。这一类通常是 R&D expense(operating expense,不是 COGS),不过当 resulting model 有明确 useful life 时,有些公司会把 fine-tuning costs 资本化为 intangible assets。资本化选择很重要:capitalized costs 不会降低 current-period earnings,而 expensed costs 会降低。

Internal-use compute:员工使用 AI tools 的成本(engineering productivity、customer support tooling、sales enablement)。无论金额大小,这都属于 operating expense,不是 COGS。

AI-native 公司的结构性问题,是 production compute 和 product-development compute 之间的灰区。团队运行 evaluation pipeline 时,可能同时在做两件事:产生改善 future model performance 的数据(R&D),并验证当前 production model(可能属于 COGS)。清晰、记录成文并一致执行的 allocation policy,是审计师会要求的东西。

另一个会计问题是 prepaid compute commitments。公司为了折扣价格向 cloud providers(AWS Bedrock、Azure OpenAI、GCP)承诺大额 compute purchase 时,会按任何 prepaid expense 的方式处理:在 balance sheet 上记为 asset,随着 compute consumed 计入 COGS。公司购买一年或三年 reserved capacity 时,处理更复杂,可能涉及 ASC 842 下的 embedded leases。

虚构 walkthrough。 想象 AgentCo,一家 $5M ARR 的 AI agent platform。公司每年花 $2M compute:$1.5M 用于 production inference(服务 customer requests),$300K 用于 training 和 evaluation,$200K 用于 internal employee tooling。正确分类下,$1.5M 进入 COGS(对 $5M revenue 的 gross margin 为 70%),$300K 是 R&D expense,$200K 是 general operating expense。若创始人错误地把全部 $2M 放入 COGS,会报告 60% gross margin,这个数字显著更差并误呈现业务。若创始人错误地只把 production inference 放入 COGS,却排除了确实服务 customer requests 的一部分 inference compute(也许团队把 evaluation runs 批处理到同一 GPU pool 上),则会夸大 gross margin。两种错误在规模化后都会放大;任何一种都过不了审计师第一次 review。

Example。 Confirmed pattern:每家 AI-native 公司都必须制定 compute-COGS classification policies。Bessemer Cloud Index 和 a16z 关于 AI margins 的文章都提到,在比较 AI-native company margins 时,一致的 compute classification 非常重要。Public AI companies(当它们大量出现时)必须详细披露 classification policies。

Primary risk。 不一致分类掩盖 margin trends。公司 Q1 用一种方式分类 compute,Q3 用另一种;结果 margin numbers 不可比;投资人失去信心。Mitigation:正式记录 classification policy;一致执行;在第一次 audit cycle 中与审计师 review。

Secondary risk。 过度资本化 development compute 以抬高短期 earnings。有些公司把 model training 和 fine-tuning costs 资本化为 intangible assets,这会改善短期盈利,但代价是 future earnings(capitalized costs 会在 asset useful life 内 amortized)。激进资本化是常见 audit-comment area。Mitigation:对 capitalization 保守处理;除非有清晰、记录成文的资产处理依据,否则大多数 development compute 应费用化。

First move。 列出公司发生的每项 compute cost。把每项分到 production / product-development / internal-use。用一页 policy memo 记录分类规则。从现在起一致执行。

Approach 8 — Cohort Analysis with Model-Cost Decay

Maturity:Emerging。Beginner difficulty:Advanced。

白话解释。 Cohort Analysis 会随时间追踪同一时期获得的 customer groups:它们的 revenue、retention 和 gross margin 随年龄如何变化。传统 SaaS cohort analysis 假设 unit costs 稳定:2023 年获得的客户,到 2026 年服务成本与 2023 年大致相同,因此 cohort 的 gross margin 稳定。

对 AI-native 公司,这个假设在结构上是错的。Foundation-model prices 已经连续几年每年下降 30–60%,并仍在下降 [Emerging pattern: 观察自 2023–2026 年主要 foundation-model providers;下降率由竞争、硬件改进和 architecture innovation 驱动,但没有任何一项保证以同样速度持续]。一个 2023 年获得、毛利率 50% 的 customer cohort,到 2026 年可能以 70% 毛利率运行,不是因为 cohort 做了任何不同的事,而是因为它消耗的 compute 更便宜了。AI-native cohort analysis 必须明确建模这种 model-cost decay,把「价格变化带来的 cohort improvement」与「客户行为带来的 cohort improvement」分开。

这是本目录中分析上最成熟的 approach 之一。它需要 data infrastructure、finance discipline 和早期公司通常还没有的耐心。但做对的公司,会比忽视它的公司更清楚地看到自己的 unit economics。

最适合作为一项随公司成熟逐步发展的 discipline,到 Series B 时变得 essential。在 usage-based 和 outcome-based pricing models 中最强,因为 compute 是成本中的重要部分。

核心想法。 随时间追踪 customer cohorts,并把 cohort behavior(retention、expansion)贡献与 falling model costs(compute price decay)贡献分开,从而理解真实的底层 unit economics。

适用场景。 当公司已有至少 12–24 个月客户数据,并且 measurement 一致。当 compute 是成本中有意义的一部分(通常为收入的 20%+)。当 finance team 拥有按 cohort 随时间追踪 gross margin 的 data infrastructure。

机制。 带 model-cost decay 的 cohort analysis 会分离传统 cohort analysis 混在一起的两个效应。

Cohort behavior effect:这个 cohort 是否留存、扩张、流失?Heavy users 是否变得更 heavy?Light users 是否掉队?这些是传统 cohort analysis 提出的问题,仍然非常关键。

Model-cost decay effect:服务这个 cohort 的成本自 acquisition 以来发生了什么变化?如果 foundation-model prices 在 cohort acquired 后下降 40%,即使 customer behavior 完全没有变化,这个 cohort 的 gross margin 也会相应改善。

方法论要求在 customer behavior 保持不变(或单独衡量其变化)的前提下,把 margin changes 归因给 compute-price decay。多数公司会维护一个「synthetic cost」baseline,也就是该 cohort 按 original acquisition-period prices 会产生的成本,并把 actual current cost 与 synthetic baseline 比较。差值就是 model-cost decay benefit,可能非常大。

战略含义是,AI-native 公司有一个传统 SaaS 没有的内置 margin tailwind。今天获得的 cohorts 在 2028 年会比今天更赚钱,即使 customer behavior 没有变化,因为 compute 会更便宜。明确建模这个效应的公司,能在 CAC payback(可接受比传统 SaaS norms 更长,因为 cohort 会随时间更赚钱)、pricing reductions(公司可以随时间降价以推动 growth 而不牺牲 margin)和 capital allocation(compute-cost-decay 是真实的 margin expansion 形式,会与 revenue growth 竞争 margin driver)上做出更好决策。

虚构 walkthrough。 想象 Sigma,一家 $10M ARR、采用 usage-based pricing 的 AI 公司。2024 cohort acquisition 时平均 gross margin 为 55%。到 2026 年初,同一 cohort 以 72% gross margin 运行。朴素解释是:「cohort 扩张 usage,变得更赚钱了。」带 model-cost decay 的 cohort analysis 显示,customer behavior 只产生了少量变化(来自 increased usage 和 small price increases 的 7% margin contribution),主导效应是 model-cost decay(foundation-model prices 下降贡献 10% margin)。Sigma 现在可以做有依据的决策:保持价格,让 margin 继续扩张;降价,用 cost decay 加速 growth;或把 margin tailwind 投入 feature expansion。没有这项分析,Sigma 可能会错误地把所有 margin improvement 归因于自己的 pricing power,并做出经不起下一轮 model-price competition 的决策。

Example。 Confirmed pattern:Public AI infrastructure companies 和较大的 AI-native vendors 越来越多地在内部运行这项分析。Bessemer Venture Partners 和 a16z growth team 的文章都引用了这个动态。该 discipline 仍在发展,公开 canonical case studies 很有限。

Primary risk。 把 margin improvement 过度归因于 cohort behavior,而实际原因是 model-cost decay。犯这个错误的公司会误判自己的 pricing power,设定在 compute prices 稳定后无法 defend 的 targets,并报告经不起 scrutiny 的 investor metrics。Mitigation:严谨维护 synthetic-cost baseline;在报告 cohort margin trends 时明确分解 behavior 和 decay。

First move。 选择一个大的 customer cohort。计算它 acquisition 时和今天的 gross margin。再计算如果按 acquisition-period compute prices,今天的 gross margin 会是多少。差值就是该 cohort 的 model-cost decay benefit。对其他 cohorts 重复,建立完整图景。

C. Planning & capital allocation

AI-native 公司如何向前看:建模未来、分配资本,并设计能预判 AI 业务独特不确定性的合同结构。这些 approaches 在资本决策发生时最重要:fundraising、hiring sprints、infrastructure commitments、pricing changes。

Approach 9 — Pilot Economics & Contract Mechanics

Maturity:Proven。Beginner difficulty:Medium。

白话解释。 多数 enterprise AI deals 并不会一开始就签 full production contracts。它们通常从 paid pilots 开始:三到六个月、金额为 production contract 一小部分的 engagement,用来证明 AI 在客户承诺 multi-year deployment 前确实有效。Pilot economics 与 production economics 不同:delivery cost 更高(更多 hand-holding)、contract size 更小、revenue recognition timing 不同。因此 pilot economics 应有自己的 accounting 和 forecasting treatment。

正确核算 pilots 的公司,能清楚看到哪些 pilots 转为 production,哪些没有。把 pilot revenue 与 production revenue 混在一起的公司,通常会误判 pipeline health,并错误 forecast。

最适合任何运行 enterprise sales motions 的公司(Sales Catalog Motions 7、8、9、10)。对 average deal sizes 高于 $50K、pilot 是标准 entry mechanism 的公司最重要。

核心想法。 把 paid pilots 作为与 production contracts 不同的 revenue category,拥有自己的 conversion rates、delivery economics 和 forecast modeling。

适用场景。 当公司运行以 paid pilots 作为标准 entry mechanism 的 enterprise sales motion。通常适用于 average deal sizes 高于 $50K 且 sales cycles 超过 60 天的公司。

机制。 Pilot economics 有效,是因为 pilots 的运营现实与 production deployments 根本不同。一个 pilot 通常包含:较小的 contract size(projected production contract 的 10–25%)、定义明确的 success-criteria document、带有大量 customer-success engagement 的 deployment period,以及结束时的 conversion decision。财务含义会传导到多个领域。

Pilot revenue recognition:pilots 通常结构化为带有 defined deliverables 的 fixed-fee engagements。ASC 606 下 revenue recognition 跟随 deliverables:如果 AI 提供 ongoing service,通常在 pilot period 内确认;如果 pilot 被结构化为带 defined output 的 research project,则可能在 completion 时确认。Recognition pattern 取决于 contract structure。

Pilot delivery economics:相对于收入,一个 pilot 会消耗不成比例的 customer-success 和 engineering time。成功 pilots 的 direct cost 常常达到 80–120%(pilot 本身 gross margin 接近零或为负),其经济性由后续 production contract 来 justify。把 pilot delivery costs 当成 production COGS 的公司会错分类 gross margin;把 pilot costs 资本化为 customer-acquisition investment 的公司可能产生不同(也可以说更准确)的财务图景。

Pilot-to-production conversion modeling:不是每个 pilot 都会转化。2026 年成熟 enterprise AI 公司通常看到 50% 到 75% 的 pilot-to-production conversion rates [Emerging pattern: 基于 enterprise AI vendors 公开数据和 investor research;下界常见于首次 deployments,上界属于有成熟 playbooks 的 category leaders],具体取决于 buyer maturity 和 category。假设 100% conversion 的 forecasting models 会夸大 future revenue;完全忽视 pilot economics 的 models 会低估 sales motion 的运营复杂度。

Pilot revenue 是否算 ARR,这个会计问题确实有争议。有些公司把它计入 ARR,并备注 pilot composition;另一些公司排除它,只报告 production-contract ARR。投资人共识越来越倾向于排除:pilot revenue 不是「annual recurring」,因为 recurrence 取决于 conversion。在 fundraising 时把 pilot revenue 放入 ARR figures 的公司,越来越会受到 sophisticated investors 的质疑。

虚构 walkthrough。 想象 MedAI,一款面向 hospital systems 的 AI 工具。MedAI 的标准 enterprise motion 是:90-day paid pilot,费用 $50K;如果成功,则跟进 $400K/year production contract。2026 年,MedAI 签下 12 个 pilots(合计 $600K pilot revenue),其中 8 个转为 production contracts(新增 $3.2M production ARR)。朴素财务图景:$3.8M new revenue。按 pilot economics 调整后的图景:$600K pilot revenue(按交付确认,不 annualized),8 个 production conversions 产生 $3.2M new ARR,4 个没有转化的 pilots(沉没在 customer-success investment 中的成本,以及 future targeting 的教训)。67% 的 pilot-to-production conversion rate 成为影响 sales-motion design 的 tracked metric。

Example。 Confirmed pattern:多数 enterprise AI vendors(Glean、Harvey、Sierra、Cresta、Writer)都运行 pilot-first motions,并把 pilot-to-production conversion 作为 board-level metric 追踪。Accounting 和 reporting treatment 各异;sophisticated investors 在 diligence 中越来越常要求明确拆分 pilot 与 production。

Primary risk。 把 pilot revenue 包含进 ARR figures,随后在 conversion rate 变得可见时失去投资人信任。Mitigation:在所有 investor materials 中把 pilot revenue 与 ARR 分开报告。把 pilot-to-production conversion rate 作为标准 reported metric。

First move。 定义你公司商业结构中的 pilot(size threshold、duration、conversion criteria)。在账本中把 pilots 作为与 production contracts 不同的 revenue category 追踪。向董事会分别报告 pilot revenue、conversion rate 和 ARR。

Approach 10 — Forecasting Under Falling Compute Costs

Maturity:Emerging。Beginner difficulty:Advanced。

白话解释。 为 AI-native 公司构建 12–24 个月 financial forecast,需要明确建模传统 SaaS forecasts 会忽略的一件事:决定你 COGS 的 foundation-model prices 会在 forecast period 内显著下降。假设 compute prices 不变的 2026-period forecast,会在结构上出错:它会低估 out-quarters 的 margin,产生误导性的 runway projections,并误导战略决策。

在 falling compute costs 下做 forecast,需要在 customer-revenue model layer 旁边建立一个单独的 compute prices model layer。两者结合,产生反映业务真实经济轨迹的 gross margin 和 contribution margin forecasts。

最适合任何有 meaningful compute spend 的公司(通常为收入的 20%+)。对正在准备重大 capital decisions 的公司最重要(Series A、Series B、大规模 hiring sprints、infrastructure commitments)。

核心想法。 用两个明确 layer 构建 forecast:customer-revenue model 和 compute-price model,并结合它们产生能预判 foundation models falling-cost trajectory 的 margin projections。

适用场景。 当公司 compute spend 超过收入的 20%。当 forecast period 长于 12 个月。当重大 capital decisions 即将发生(fundraising、大规模招聘、infrastructure commitments)。

机制。 传统 SaaS forecast model 有一个 revenue layer(subscription growth、churn、expansion)和一个 cost layer(compute、sales、marketing、R&D、G&A)。Compute 通常被建模为 revenue percentage,或 fixed-cost-plus-growth model。

AI-native forecast model 会加入第三层:compute-price model。这个 layer 预测 forecast period 内 foundation-model prices 将如何演化。标准方法使用 observed price decay rates(2023 到 2026 年主要 model providers 通常每年 30–60%),并向前投影,同时对 assumed decay rate 做 sensitivity analysis。

组合后的 forecast 会产生经常令人意外的 gross-margin trajectories。一家公司今天 55% gross margin 持平,可能在 18 个月后 forecast 65% gross margin,36 个月后 forecast 70% gross margin,而原因完全来自 compute-price decay,不需要改变 customer pricing 或 behavior。这会创造 flat-margin forecast 看不到的 strategic options:降价以推动 growth(margin tailwind 吸收影响)、扩大 feature investment(future cost base 更低),或只是向投资人提出更高但可信的 target margins。

最常见 failure mode 是对 compute-price decay rate 过度乐观。2023 到 2026 年 foundation-model prices 快速下降,但这个速度并不保证持续。Decay 由 provider competition(可能稳定)、类似 Moore's Law 的 hardware improvements(正在放缓)和 architectural innovations(不可预测)驱动。成熟 forecast models 会包含多个 scenarios:aggressive decay(50%/year)、base case(30%/year)和 conservative(10%/year),并明确 sensitivity analysis。

另一个约束是系统性追踪 compute prices 的 data infrastructure。Foundation-model providers 会频繁改变 pricing;公司必须跨 providers 监控变化,记录 price trajectory,并随 pricing changes 更新 forecasts。试图在 spreadsheets 里做这件事的公司通常会落后;把 tracking 建进 FP&A infrastructure 的公司才能保持 current。

虚构 walkthrough。 想象 GenStudio,一家 $8M ARR 的 AI image-generation 公司,annual compute spend 为 $3M(收入的 37.5%,毛利率 62.5%)。团队正在为 Series B fundraise 做 18 个月 forecast。传统 forecast 假设 compute costs 保持在 revenue 的 37.5%;18 个月后 projected gross margin 仍为 62.5%,公司预计达到 $30M ARR。加入 compute-price-decay layer 后(base case 假设 35%/year decay rate),18 个月后 projected compute spend 是 $3M × (1 − 0.35)^1.5 ≈ $1.5M,对应 projected $30M revenue,gross margin 为 95%。这个数字高得不现实;模型需要 refinement(usage 很可能随 revenue 增长,部分抵消 decay benefit)。现实图景大约落在 18 个月后 70% 到 80% gross margin 之间。无论如何,forecast picture 与朴素 flat-margin assumption 明显不同,战略含义也不同。

Example。 Emerging pattern:准备 Series B 及以后融资的 sophisticated AI-native 公司,越来越明确地建模 compute-price decay。这个 discipline 太年轻,还没有广泛公开的 case studies,但 Bessemer 和 a16z 都发表过引用该动态的研究。Public companies(当它们更多出现时)会在 forward guidance 中面对投资人对 compute-price assumptions 的问题。

Primary risk。 对 decay rate 过度乐观。Aggressive decay assumptions 会产生乐观 forecast,无法承受真实 pricing dynamics。Mitigation:建模多个 scenarios(aggressive、base、conservative);runway planning 用 conservative case,strategic targets 用 base case。

First move。 计算过去六个季度中每个季度 compute spend 占 revenue 的百分比。记录这段时间影响成本的 foundation-model price changes。用 base-case decay rate 向前投影(30%/year 是合理起点),并在 ±20% 做 sensitivity analysis。

Approach 11 — Capital Allocation

Maturity:Proven。Beginner difficulty:Medium。

白话解释。 Capital Allocation 是战略问题:如何把公司新增 dollars 分配到相互竞争的需求上:更多 compute 来扩张产品,更多 engineers 来交付 features,更多 salespeople 来增长 revenue,更多 marketing 来填充 funnel,或更多 cash reserves 来延长 runway。AI-native 公司做出的每一个重大财务决策,本质上都是某种形式的 capital-allocation decision。

让 AI-native capital allocation 不同于传统 SaaS 的维度,是 compute spend curve。Compute 是随 usage 扩张的 variable cost,但它也受到团队如何积极优化的战略选择影响。同样的 dollars,团队可以花在更多 compute 上,以当前效率服务更多客户;也可以花在 engineering work 上,降低 per-call compute cost,从而扩大 future margins。「以当前效率 scale」和「投资 efficiency」之间的取舍,是传统 SaaS 不需要以同样强度面对的战略决策。

最适合作为随公司规模逐步发展的 discipline,到 Series A 变得 essential,到 Series B 成为核心。

核心想法。 把每一美元增量资本都视为 compute、people、customer acquisition 和 runway 之间的战略选择,并明确框架说明如何选择。

适用场景。 从 Series A 开始,当公司有足够资本,需要系统性 allocation,而不是 ad-hoc spending decisions。最重要的时刻是 capital base 发生变化时(fundraises、大客户付款、M&A)。

机制。 2026 年多数 AI-native 公司面对四类增量资本需求。

Compute:支付更多 foundation-model API calls、更多 GPU rentals、更多 training runs、更多 inference capacity。如果架构不变,compute spend 会大致随 revenue 增长;如果公司加入更多 compute-intensive features,则会比 revenue 增长更快。

People:雇更多 engineers、sales reps、marketers、customer-success professionals。People spend 会随公司复杂度增长;成熟 SaaS 中的经验法则是,在美国主要 tech hubs,每位员工 fully loaded 每年大约 $200K–$400K(salary、benefits、equipment、allocated overhead)。

Customer acquisition:paid marketing、sales-development resources、partnership investments、channel programs。CAC spend 会随 growth ambitions 增长;问题是 LTV/CAC math 是否 justify 这笔 spend。

Runway:留在 balance sheet 上的现金。Runway 有战略价值:它让公司有 optionality 去 pivot、度过 downturns,并避免在不利条款下融资。多数公司在 growth phases 低估 runway;也有些公司过度重视 runway,饿死 growth investments。

这里的关键战略概念是 Burn Multiple(由 David Sacks 推广):cash burned 与 net new ARR added 的比率。一家公司 annual burn 为 $5M,同时新增 $5M ARR,则 Burn Multiple 是 1.0;越低越好。成熟 SaaS norms 认为健康 Burn Multiple 应为 1.5x 或更低 [Industry benchmark];AI-native 公司因 compute-cost component 往往更高,在 early-stage growth-mode companies 中 2.0x 也被视为可接受 [Emerging pattern]。

传统 SaaS 不需要面对的 AI-specific capital-allocation 问题,是是否投资 compute efficiency 还是 product scaling。Engineering time 用于优化 prompts、batching inference、distilling smaller models,或构建 custom inference infrastructure,可能带来有意义的 margin improvements(通常 per-call costs 降低 20–40%)。但同样的 engineering time 也可以用于交付推动 revenue growth 的 features。正确答案取决于公司阶段、margin opportunity 的量级,以及客户对新 features 的 pull。

虚构 walkthrough。 想象 FlexAI,一家刚获得 $50M 新资本的 Series B AI 公司。Leadership team 必须在四类需求之间分配资本。基于标准 SaaS playbooks 的默认 allocation 可能是:$20M 给 people growth(扩张 sales 和 engineering),$15M 给 customer acquisition,$10M 留作 runway,$5M 给 compute。AI-native-aware allocation 可能会调整为:$15M 给 people growth,$12M 给 customer acquisition,$10M 给 compute(预判 revenue growth),$8M 给 compute-efficiency engineering,$5M 给 runway。从 $5M 到 $8M 的 efficiency engineering 变化,反映了一个战略押注:未来 $100M revenue base 上 30% margin improvement 每年价值 $30M;即便前期投入很大,这个 payoff 也 justify。

Example。 Confirmed pattern:准备 Series B 及以后 capital-allocation plans 的 AI-native 公司,越来越明确地权衡 compute-efficiency engineering 和其他 capital uses。公开讨论有限;实践更多记录在 board meetings 和 capital plans 中,而不是 published reference 中。

Primary risk。 Compute over-investment。公司过度分配资本给 compute capacity,造成 capacity 超过 demand,并压低 margins。Mitigation:按 demonstrated demand 分配 compute capacity,并设定明确 scale-up triggers,而不是提前承诺 capacity。

Secondary risk。 Compute-efficiency under-investment。公司没有投入 compute efficiency,把 20–40% margin improvements 留在桌面上。Mitigation:每季度 review compute-efficiency engineering opportunities;明确分配 engineering capacity,不让 feature work 挤出 efficiency work。

First move。 为公司建立一页 capital-allocation framework。识别竞争资本的四类(或更多)需求。记录指导 allocation 的原则。每季度 review 该 framework。

D. 外部报告

公司如何与投资人、董事会和审计师沟通。AI-native 公司报告的 metrics、dashboards 和 disclosures 与传统 SaaS norms 有显著不同。

Approach 12 — Investor & Board Reporting

Maturity:Proven。Beginner difficulty:Medium。

白话解释。 Investor & Board Reporting 是把公司财务状态提炼为投资人、董事会成员和审计师期待看到的 metrics、dashboards 和 narratives 的 discipline。对传统 SaaS,canonical metrics 已经很成熟:ARR、NRR、gross margin、CAC payback、Burn Multiple、Magic Number。对 AI-native 公司,同样的 metrics 仍然适用,但必须补充传统 SaaS 不需要的 AI-specific metrics。

只报告传统 SaaS metrics 的公司,会生成错过 AI-native dynamics 的财务图景:model-cost decay、outcome-attribution risk、pilot-to-production conversion、compute-as-percentage-of-revenue。只报告 AI-specific metrics 的公司,又无法与传统 SaaS benchmarks 做有意义比较,也会让锚定这些 benchmarks 的投资人困惑。正确答案是两者都报告,并明确说明这些 metrics 如何关联。

最适合作为随公司成熟逐步发展的 discipline。在 fundraising、board meetings 和 audit cycles 中最重要。

核心想法。 报告所有投资人都期待的 canonical SaaS metrics,同时补充捕捉传统 SaaS 不具备动态的 AI-specific metrics。

适用场景。 从 Series A 开始。Pre-revenue 公司可以推迟其中大部分,不过基础 burn-and-runway reporting 从公司成立就开始。

机制。 一份完整的 AI-native 公司财务报告,通常会包含以下 metrics,并组织成三层。

Tier 1 — 任何 subscription-flavored business 的投资人都期待的 canonical SaaS metrics。ARR(annual recurring revenue)、NRR(net revenue retention)、GRR(gross revenue retention)、gross margin、contribution margin、CAC payback period、Burn Multiple、cash runway in months。这些是 baseline;每个投资人都会问,AI-native 公司要像任何 SaaS 一样报告。

Tier 2 — 捕捉 AI-native dynamics 的 AI-specific metrics。Compute as percentage of revenue(最重要的 AI-specific margin metric,当前 AI-native 公司通常为 20–60%)。Cohort gross margin trend(margins 是否随时间改善,并在 behavior 和 model-cost decay 之间拆分)。Pilot-to-production conversion rate(对运行 enterprise sales motions 的公司)。Outcome attribution accuracy(对 per-outcome pricing 公司,即团队能用 audit-grade telemetry defend 的 contracted outcomes 百分比)。Bookings vs. recognized revenue(对有 non-subscription contracts 的公司,即 contracted value 与 GAAP revenue 之间的 gap)。Model-cost-decay benefit(归因于 foundation-model prices 下降的 margin improvement,并与 cohort behavior 分离)。

Tier 3 — AI-native 公司经常加入的 strategic context。Compute concentration risk(单一 foundation-model providers 中 compute spend 的百分比,捕捉对 Anthropic、OpenAI 等的依赖)。Forecast accuracy(过去 4–8 个 quarters 的 actuals vs. forecast,展示团队 predictive maturity)。Capital allocation breakdown(incremental capital 如何在 compute、people、acquisition 和 runway 之间分配)。

约束是 reporting overhead。每月产出一份完整报告需要有意义的 FP&A capacity;按季度产出有深度的报告,需要 controller 和 senior analyst。试图每月报告一切的公司,通常产出很浅;按季度深度报告的公司,产出更有用的报告。

虚构 walkthrough。 想象 GrowthAI,一家 Series B AI 公司。它们的季度 board report 包含 Tier 1 metrics(ARR $25M、NRR 130%、gross margin 65%、Burn Multiple 1.4x、runway 24 months)、Tier 2 metrics(compute 从一年前 revenue 的 35% 降到 28%、cohort gross margin 每季度上升 2 points 且有明确 decomposition、pilot-to-production 70%),以及 Tier 3 context(90% compute spend 分布在两个 providers、过去八个 quarters forecast accuracy 为 ±8%、$50M capital deployment plan)。报告 12 页,每个 metric 都有明确 narrative。投资人和董事会成员 30 分钟内能读完,并在会议中提出有信息量的问题;重要 dynamics 可见,不需要董事会成员自己挖。

Example。 Confirmed pattern:正在准备或已经进入 Series B 及以后阶段的 sophisticated AI-native 公司,越来越多地产出包含 Tier 2 和 Tier 3 metrics 的报告。格式各异,但底层 discipline 在不同公司之间相似。

Primary risk。 Vanity metrics over substance。团队报告听起来漂亮的数字(signed bookings、total contract value、total registered users),但这些数字不反映底层业务状态。Mitigation:先把 reporting 锚定在 cash、recognized revenue 和 gross margin;只有在明确 context 下再补充 bookings 和 pipeline。

First move。 列出上一份 board report 包含的 metrics。与上面的 Tier 1、Tier 2 和 Tier 3 列表比较。找出两三项真正会改善报告的新增指标。

E. 指标与 KPI 框架

前四节覆盖 AI-native finance 做什么(price、account、plan、report)。本节覆盖 AI-native finance 衡量什么:决定 AI-native 公司是否成功的具体 metrics 和 KPIs,并组织成一个 hierarchy,从 operational layer(per-AI-worker performance)一路到 unit-economics layer(per-customer 或 per-outcome profitability),再到 company-level financial layer(gross margin、ARR、runway),最后到 investor-facing layer(Burn Multiple、capital efficiency)。

本节是目录中最具处方性的部分。前面的 approaches 给你 architecture choices;本节给你应该实际追踪的数字、计算公式、区分健康与不健康的 thresholds,以及一家 $10M ARR AI-native 公司的 worked example dashboard。

指标层级

每家 AI-native 公司的财务现实,都会从四层 metrics hierarchy 中浮现。每一层都会馈入上一层。

Layer 1 — AI Worker operational metrics。 AI 本身的 performance:outcomes produced、accuracy、escalation rates、throughput。这些是 engineering 和 product metrics,传统 finance 通常不参与;但对 AI-native 公司,它们是每个财务数字的 upstream drivers。一个 90% outcome rate、5% escalation rate 的 AI Worker,与一个 60% outcome rate、35% escalation rate 的 AI Worker,会产生完全不同的 unit economics,不管合同如何定价。

Layer 2 — Unit economics。 Per-customer 或 per-outcome profitability。Contribution margin per outcome、gross margin per call、customer LTV、CAC per cohort、LTV/CAC ratio。这些 metrics 会把 Layer 1 operational performance 转换为财务信号:高 escalation rate(Layer 1)会表现为低 gross margin per outcome(Layer 2)。

Layer 3 — Company-level financial metrics。 公司的 aggregate financial state。ARR、NRR、gross margin、contribution margin、cash burn、runway。这些是 income statement 和 cash-flow report 上的 metrics,也就是业务的 GAAP view。它们汇总了所有客户和所有时期的 Layer 2 unit economics。

Layer 4 — Investor and capital-efficiency metrics。 用来把公司与 benchmarks 比较、驱动 valuation、指导 fundraising 的 metrics。Burn Multiple、Magic Number、Rule of 40、ARR per employee、capital efficiency ratios。这些 metrics 源自 Layer 3 financials,但强调 efficiency 和 benchmarking,而不是 absolute performance。

对 AI-native finance teams 的关键 insight 是:只报告 Layer 4 metrics(最容易产出)的公司,其实是在看不见真正驱动业务的因素。诊断信息位于 Layers 1 和 2;战略叙事位于 Layer 3;investor pitch 位于 Layer 4。成熟 finance functions 会报告全部四层,并明确连接它们之间的因果关系。

AI Worker operational KPIs

Layer 1 metrics,也就是 AI 本身的 performance,是最新、也是传统 finance literature 最少覆盖的部分。可它们是每个 financial KPI 的 upstream drivers。追踪得好的公司,会比这些趋势进入 P&L 早三到六个月看到 gross-margin trends;忽视它们的公司,只能被动面对自己解释不了的 financial outcomes。

六个核心 AI Worker operational metrics 适用于大多数 worker types:

1. Outcome rate。 尝试中产生 successful outcome 的百分比。对 customer-support AI:resolved without escalation 的 tickets 除以 total tickets received。对 sales-outreach AI:booked meetings 除以 total messages sent。对 code-generation AI:human reviewer 接受的 generated code 除以 total generation attempts。

Outcome rate = Successful outcomes / Total attempts

健康区间会因 worker type 大幅不同。Customer support:60–85%。Sales outreach:2–15%(低得多,因为 buyer-side response rate 是瓶颈)。Code generation:30–70%。Baseline 是 human-only rate;如果 AI Worker 能以显著更低成本持续超过 baseline,就说明它在成功。

2. Quality。 AI 产生 outcome 的 human-rated 或 auditor-rated quality。对 customer support:post-resolution customer satisfaction(CSAT)scores。对 document analysis:audit sample 中被标记为 correct 的 analyzed documents 百分比。对 meeting summarization:decisions 和 action items 被正确捕捉的百分比。

Quality = Average rated score (1–5 or 1–10 scale) across audited outcomes

Outcome rate 和 quality 之间的 gap 在运营上非常重要。一个 90% outcome rate、60% quality score 的 AI,会产生大量技术上算作「outcomes」的坏结果。两个 metrics 放在一起才给出真相。

3. Throughput。 单位时间产生的 outcomes。每小时 resolved tickets、每分钟 generated summaries、每天 processed claims。与同一 workflow 中的人类 throughput 比较时,throughput 才具有财务意义;这个倍数就是 automation leverage。

Throughput = Outcomes / Time period

Automation leverage = AI throughput / Human throughput

执行结构化任务(claims、document analysis、simple support)的典型 AI Worker,相比人类 equivalent 会有 5–20x automation leverage。执行 creative 或 judgment-heavy tasks 的 AI Workers 通常为 2–5x。需要 AI 无法访问的 context 的 tasks,automation leverage 接近 1x,通常不应部署。

4. Reliability。 AI Worker performance 的一致性:uptime、error rate、异常 inputs 下的 behavior。它包括 infrastructure reliability(uptime)和 behavioral reliability(相似 inputs 上 outcomes 的一致性)。

Reliability = (Uptime %) × (1 − Error rate) × (Behavioral consistency score)

Reliability 决定 AI Worker 是否可以被信任并进入 production。一个 outcome rate 很高、但相似 inputs 上 behavior 变化很大的 AI,即使 average performance 很好,也不能部署到 regulated industries。

5. Cost per outcome。 产生一个 outcome 的 fully-loaded cost,包括 foundation-model API costs、supporting infrastructure、monitoring,以及按比例分配的 engineering 和 customer-success time。

Cost per outcome = (Compute cost + Infrastructure cost + Allocated overhead) / Total outcomes produced

这是 finance 最重要的 Layer 1 metric,因为它直接驱动 gross margin per outcome(Layer 2)。Customer-support AI 的典型区间是每张 resolved ticket $0.20–$0.80。Sales-outreach AI:每次 booked meeting $0.50–$3。Code-generation AI:每条 accepted code suggestion $0.10–$1。

6. Cost-per-outcome trend。 Cost per outcome 随时间变化的速度。随着 foundation-model prices decay(每年 30–60%)、团队优化 prompts,以及 caching 和 batching 提升效率,它应该随时间下降。持平或上升的 trend 表示有问题,可能原因包括:model-cost-decay benefits 没有被捕获(仍在用更贵的 models)、workflow drift(AI 被要求做越来越难的事情),或 infrastructure inefficiency。

Cost-per-outcome trend = (Cost per outcome this period − Cost per outcome prior period) / Cost per outcome prior period

健康 AI Worker 的 cost-per-outcome 每年下降 20–40% [Author thesis: 来自 observed model-price decay 加典型 prompt-optimization gains;应以你自己的 deployment 数据验证]。这个 decay 是 Approach 8 中 model-cost-decay margin tailwind 的运营侧对应物。

这六个 metrics 合在一起回答运营问题:这个 AI Worker 是否成功,它以多大 margin 成功,成功是否随时间改善?对 production 中每个 AI Worker 追踪这些 metrics 的公司,会提前看到 margin issues、customer-success problems 和 competitive pressure。不追踪的公司,会在三到六个月后从 financial statements 中得知同样问题,那时已经更难修复。

Per-architecture financial KPIs

Section A 中每种 pricing architecture 都有自己的 financial KPIs,用来判断该 architecture 是否有效。Metrics 有重叠,但重点不同。

Per-Seat Pricing KPIs。 当 revenue 随 seats 扩张时,重要 metrics 是:

- Seats sold(gross)、seats churned(gross)、net seats added:任何 per-seat business 的基础 flow metrics

- Seat utilization rate:paid seats 中有 monthly active usage 的百分比;健康区间为 60–85%,低于 50% 表示存在大量 billing-without-value 风险

- ARPU(Average Revenue Per User):total revenue 除以 active users

- ARPA(Average Revenue Per Account):total revenue 除以 paying accounts

- Compute cost per seat:AI-specific addition;这是 heavy users 带来 margin compression 的主要 indicator

- Compute-cost-per-seat distribution:heavy/medium/light user breakdown;如果 heavy-user compute 超过 seat revenue 的 80%,architecture 需要演化

Seat utilization rate = Active users / Paid seats

ARPU = Total revenue / Active users

Compute cost per seat = Total compute cost / Paid seats

Per-Call / Usage Pricing KPIs。 当 revenue 随 consumption 扩张时,重要 metrics 是:

- Active customers:该期间有任何 billable usage 的客户

- Calls per active customer:每个客户的 usage intensity

- Revenue per call:所有 billable calls 的 average revenue

- Gross margin per call:(Revenue per call − Cost per call) / Revenue per call;结构上应保持 60%+

- Customer concentration:top 5/10/20 customers 贡献收入百分比;top 5 超过 30% 表示 concentration risk

- Usage growth rate:每个客户 calls 的 month-over-month 增长;早期产品阶段健康区间为 5–15% MoM

- Bill-shock churn rate:明确因 billing surprise 而 churn 的客户;超过 5%/year 表示 bill management 的 customer success 不足

Calls per active customer = Total billable calls / Active customers

Gross margin per call = (Revenue per call − Cost per call) / Revenue per call

Customer concentration (top 5) = Revenue from top 5 customers / Total revenue

Per-Outcome Pricing KPIs。 Outcome-based architectures 的 specific metrics:

- Outcomes delivered per period:volume metric;revenue 的 upstream driver

- Outcome attribution accuracy:团队能用 audit-grade telemetry defend 的 delivered outcomes 百分比;应为 95%+

- Outcome dispute rate:customers dispute 的 billable outcomes 百分比;超过 3% 表示 attribution-infrastructure problems

- Average revenue per outcome:公司每个 outcome 捕获的 price

- Cost per outcome:每个 outcome 的 total cost(compute + supporting infrastructure + allocated overhead)

- Contribution margin per outcome:(Revenue per outcome − Variable costs per outcome) / Revenue per outcome

- Customer outcome consumption growth rate:按客户追踪 usage trajectory

Contribution margin per outcome = (Revenue per outcome − Variable costs per outcome) / Revenue per outcome

Outcome attribution accuracy = Outcomes with audit-grade telemetry / Total outcomes billed

Value-Based Pricing KPIs。 最成熟 architecture 的 metrics:

- Baseline measurement period results:客户 deployment 前的 metrics

- Measured value vs. baseline:驱动 billing 的 gap

- Value-share capture rate:vendor 对 measured gap 的 share;通常为 5–25%

- Audit completion rate:完成 audit cycles 的合同百分比;低于 80% 表示 audit-rights infrastructure broken

- Variable consideration recognition rate:contracted upside 中实际确认为 revenue 的百分比;早年因 ASC 606 conservatism 可能低至 30–50%,随着 track record 成熟而上升

- Customer renewal rate at contract end:这类合同有天然 expiration cliffs;renewal rate 是 durability test

Hybrid Pricing KPIs。 多个 components 组合时的重要 metrics:

- Subscription-vs-usage revenue split:每个 component 的 revenue 百分比;追踪 mix 如何演化

- Overage rate:超过 included quota 的 customers 百分比;健康区间 30–60%,表示 pricing 校准正确

- Average overage revenue per overage customer:heavy users 带来的 upside

- Conversion to higher tier:overage customers 升级到更高 subscription tiers 的百分比

- Bill predictability score:每个客户 monthly bills 的 variance;variance 越低,churn 越低

各阶段指标优先级

不同指标在公司成熟度的不同阶段重要性不同。Pre-revenue 公司沉迷 Burn Multiple 是浪费时间;Series B 公司还停留在追踪 ARR,则报告太薄。

Pre-revenue(Seed)。

Top 3 metrics:cash runway(以月计)、monthly burn(dollars)、lead indicators(waitlist signups、design-partner conversations、beta users)。其他都跳过。ARR、NRR、gross margin、CAC 还没有意义:数据太少,pattern 下个季度就会变化,把时间花在计算上不如赢得下一个客户。

Early revenue($1M–$5M ARR)。

Top 5 metrics:ARR、gross margin(明确 compute-cost line)、cash runway、NRR(gross + net)、CAC payback period。开始追踪;还不要优化。这些 metrics 建立 Series A diligence 所需 baseline;第一年的 values 没有 trajectory 和团队解释能力重要。

Mid stage($5M–$25M ARR)。

Top 7 metrics:以上 metrics 加上 Burn Multiple、contribution margin、pilot-to-production conversion(如果是 enterprise sales motion)、compute as percentage of revenue。开始重要:带 model-cost decay 的 cohort analysis、customer concentration。从「tracking metrics」到「optimizing metrics」的转变发生在这个阶段;finance function 从 scorekeeping 变成 strategic input。

Scaling($25M+ ARR)。

Approach 12 中的完整 Tier 1、Tier 2 和 Tier 3。所有 metrics 都重要。战略问题是 reporting cadence:哪些 metrics 每周 review(cash、pipeline、top-customer health),哪些每月 review(full P&L、gross margin trends、cohort analysis),哪些每季度 review(包含三层的 full investor report),哪些每年 review(audit、full strategic financial review)。

最常见的 stage-related mistake,是在 Series A 规模报告 Series B metrics。一个 pre-product-market-fit 公司做出 14 页 board deck,包含 cohort analyses、capital efficiency ratios 和 Rule of 40 calculations,其实是在表演 finance theater。董事会想看 runway、burn 和 customer count;其他在这个阶段都是 overhead。

AI-specific operational efficiency KPIs

这些是 engineering-finance bridge metrics:engineering 和 finance 必须一起追踪,因为它们直接决定 unit economics。传统 SaaS finance 不参与这些,是因为 hosting costs 太小而不重要;AI-native finance 必须参与。

Cost per token(input vs. output)。 Foundation-model API calls 的 unit cost。分别追踪 input tokens(prompt)和 output tokens(response),因为不同 providers 的 pricing 可相差一个数量级。随时间追踪,因为 foundation-model pricing 频繁变化;季度快照会错过动态。

Inference cost per query。 Total compute cost(foundation-model API + supporting compute)除以 total queries served。最重要的 AI-specific operational metric,因为它直接决定 gross margin per call(Layer 2)。

Inference cost per query = (Foundation-model API cost + Supporting compute cost) / Total queries served

Cache hit rate。 对有 response caching 的系统,requests 中从 cache 服务、而不是需要 full inference 的百分比。30% cache hit rate 会带来有意义的 cost savings;60%+ cache hit rate 会改变 unit economics。

Batch processing efficiency。 对可 batch 的 workloads(overnight processing、retry queues、bulk operations),batched 与 real-time 的 cost per outcome。Batched costs 通常比 real-time 低 50–80%;未 batch 符合条件 workloads 的公司,会把大量 margin 留在桌面上。

Model utilization rate。 对 self-hosted infrastructure,GPU utilization percentage。低于 40% 表示 over-provisioned infrastructure;持续 80%+ 表示 capacity-planning 需要关注。

Prompt token efficiency。 每个 input token consumed 产生的 output value。它衡量 prompt design quality:高效 prompts 用最少 input context 产生高价值 outputs。

Time-to-first-token / time-to-completion。 影响 customer experience 的 performance metrics;对某些 workloads,它们决定 AI Worker 是否能与 human alternatives 竞争。

Capital efficiency metrics beyond Burn Multiple

Burn Multiple 只是更大 capital-efficiency framework 中的一个指标。AI-native 公司应追踪并报告更完整的一组:

ARR per employee。 Total ARR 除以 total full-time employees(包括折算为 FTE-equivalent 的 contractors)。这是最直接的 revenue productivity 指标。成熟 SaaS 目标为每人 $200K–$400K;$5M–$25M ARR 区间的 AI-native 公司通常为每人 $150K–$300K,因 engineering intensity 更高而略低。

ARR per employee = Total ARR / Total FTEs

Gross profit per employee。 ARR per employee 乘以 gross margin。它会调整 AI-native lower-gross-margin reality,并在 SaaS 和 AI-native 公司之间产生更可比的 metric。

Gross profit per employee = (Total ARR × Gross margin) / Total FTEs

R&D as percentage of revenue。 Research and development spend(engineering、product、design)除以 revenue。AI-native norms 在 growth phases 通常为 35–55%(高于 SaaS norms 的 25–40%),原因是 engineering intensity 以及 AI Finance Engineer / AI Outcome Engineer roles。随着公司 scale,会下降到接近 SaaS norms。

S&M as percentage of new ARR。 某一期间 sales and marketing spend 除以同一期间 net new ARR added。它是 Magic Number 的倒数;越低越好。成熟 SaaS 目标为 100–150%(每 $1 S&M dollar 在该期间产生 $0.67–$1 net new ARR);AI-native 公司早期常为 80–120%,因为 product-led acquisition 更强。

G&A as percentage of revenue。 General and administrative spend 除以 revenue。成熟 SaaS norms 为 10–15%;AI-native norms 类似。高于 20% 表示 organizational bloat 或过早 CFO/finance build-out。

Rule of 40。 Annual revenue growth rate 加 EBITDA margin。这是 canonical SaaS efficiency benchmark;成熟公司应超过 40%。Growth phase 的 AI-native 公司经常低于这个阈值(高 growth 被深 operating losses 抵消),并在 scale 后逐步达到 Rule of 40。

Rule of 40 = Annual revenue growth % + EBITDA margin %

Rule of 50/60 for fast-growing AI-native companies。 有些 AI-native investors 对 hypergrowth AI-native 公司采用 Rule of 50 或 Rule of 60,也就是接受更深 losses 来换取更快 growth。它不如 Rule of 40 普遍,但被越来越多提及。

Capital efficiency ratio。 Total ARR 除以至今 total capital raised。它衡量公司部署融资资本的生产率。成熟 SaaS 目标为 1.5x 或更高;早期 AI-native 公司常为 0.5–1.0x,并随时间改善。

Capital efficiency ratio = Total ARR / Total capital raised

Worked example: AgentCo at $10M ARR

为了让这个 framework 更具体,考虑一家 $10M ARR 的虚构 AI-native 公司。下面的 metrics 代表一家健康 mid-stage AI-native 公司;偏离这些 benchmarks 的地方,就是问题或机会的排查方向。

Company profile。 AgentCo 是一家 AI customer-support automation 公司。Pricing 是 hybrid:每客户 $5,000/month subscription(包含每月 50,000 resolved tickets),超过 included quota 后每张 ticket 收 $0.50。100 customers,average $100K ACV。50 employees。Series A close(raised $30M)后 18 个月;准备在 12–18 个月后进行 Series B。

Annual P&L。

| Line item | Amount | % of revenue |

|---|---|---|

| Bookings (signed contracts) | $14M | 140% |

| Revenue (recognized GAAP) | $10M | 100% |

| COGS | ||

| Compute (foundation-model API) | $2.5M | 25% |

| Hosting & infrastructure | $400K | 4% |

| Customer-success allocation (variable) | $600K | 6% |

| Total COGS | $3.5M | 35% |

| Gross profit | $6.5M | 65% |

| Operating expenses | ||

| R&D (20 engineers) | $4M | 40% |

| Sales & Marketing | $3.5M | 35% |

| G&A | $2M | 20% |

| Total OpEx | $9.5M | 95% |

| Operating loss | ($3M) | (30%) |

| Cash burn (after working-capital benefit) | ($2.5M) | (25%) |

| Cash on hand | $25M | — |

| Runway | 按当前 burn 为 10 years | — |

Layer 1 — AI Worker operational metrics。

| Metric | Value | Healthy? |

|---|---|---|

| Outcome rate (tickets resolved without escalation) | 78% | Yes (60–85% range) |

| Quality (CSAT post-resolution) | 4.4 / 5 | Yes |

| Throughput (resolutions per hour) | 120 | Yes (vs. human 8/hr = 15x leverage) |

| Reliability (uptime × consistency) | 99.5% × 96% = 95.5% | Yes |

| Cost per outcome | $0.42 | Yes ($0.20–0.80 range) |

| Cost-per-outcome trend (YoY) | −28% | Yes (within 20–40% target) |

Layer 2 — Unit economics。

| Metric | Value | Healthy? |

|---|---|---|

| ACV (Average Contract Value) | $100K | — |

| CAC | $50K | — |

| LTV (5-year, with 130% NRR) | $500K | — |

| LTV/CAC ratio | 10x | Excellent (target > 3x) |

| CAC payback period | 14 months | Healthy (target < 18 months) |